Credit Card Encryption | What is it ?

Roan Dollmann

October 13, 2025

1

minutes

What Is Credit Card Encryption?

Credit card encryption is a security measure designed to protect sensitive payment information.

Like a secret code that protects every transaction.

It scrambles your customers' payment details into unreadable data that only authorized systems can decode - keeping sensitive information safe from hackers and fraudsters.

When you use your card for a purchase, encryption helps scramble the details to make it unreadable to anyone who might try to steal it.

This process is crucial in preventing fraudulent transactions and ensuring your data stays secure throughout the transaction.

How Credit Card Encryption Works

Encryption works in multiple stages during a payment, ensuring payment fraud prevention at every step

It starts right at the card level, where the details are encrypted before they even leave your hands.

This makes it nearly impossible for anyone to access or misuse your payment information without the correct decryption key.

1. Protecting Your Card Information

When you make a payment, your card information is converted into a code using encryption. This makes it nearly impossible for anyone to steal or use your data without the right key.

2. The Power of EMV Chips

Today’s credit cards use EMV chips—the small square microchips on the front of your card. These chips create a unique code every time you make a purchase, making it harder for fraudsters to use your information.

3. Real-time Encryption

The encryption process happens instantly when you swipe, dip, or tap your card at the payment terminal. This ensures that your payment information is secured at the exact moment of the transaction.

4. The Risk of Magnetic Stripes

Older cards have a magnetic stripe on the back. This is less secure because thieves can steal data from it using skimmers at ATMs or gas stations. They can then use the stolen information to create fake cards.

5. How EMV Chips Protect You

Unlike magnetic stripes, EMV chips generate a one-time code (called a cryptogram) for each transaction, providing stronger fraud protection and payment data security.

This code is unique for each purchase and expires after use, so even if someone steals it, they can’t use it for another transaction.

6. Dynamic Data vs Static Data

EMV chips use dynamic data for each transaction, meaning the information changes with every purchase. In contrast, the magnetic stripe holds static data, which can be easily copied and used again by fraudsters.

7. Extra Protection with PINs or Signatures

For added security, merchants may ask for a PIN or signature (this is called chip-and-PIN or chip-and-signature). Some newer cards, like the Mastercard Biometric Card, even use your fingerprint for extra protection.

How Effective is Credit Card Encryption?

Credit card encryption has made payments significantly safer, but it's not 100% foolproof. Here's the real picture.

While EMV chips have made it harder for fraudsters to steal card information through skimming (such as at ATMs), payment fraud risks still exist.

One example is online transactions - when the cardholder enters their card number on a website, but the chip isn't involved in the process.

These are known as card-not-present transactions.

To provide extra protection for these types of purchases, online stores often ask for a CVV (card verification value) or CID (card identification number). This is a separate 3- or 4-digit code found on your card.

The CVV/CID adds another layer of security because, even if a thief has your card number, they won’t be able to complete the transaction without this extra code.

The Bottom Line:

While encryption has dramatically improved security, businesses still need multiple protections - especially for online sales.

This is why payment processors use encryption PLUS other safeguards like:

- Address verification

- Fraud scoring systems

- Two-factor authentication

⚠️Some industries face greater exposure to fraud, especially in online transactions.

That’s why combining credit card encryption with secure, compliant payment processing solutions for high-risk businesses — like those provided by FirmEU — is essential.

This approach helps protect sensitive data, reduce chargebacks, and keep transactions running smoothly.

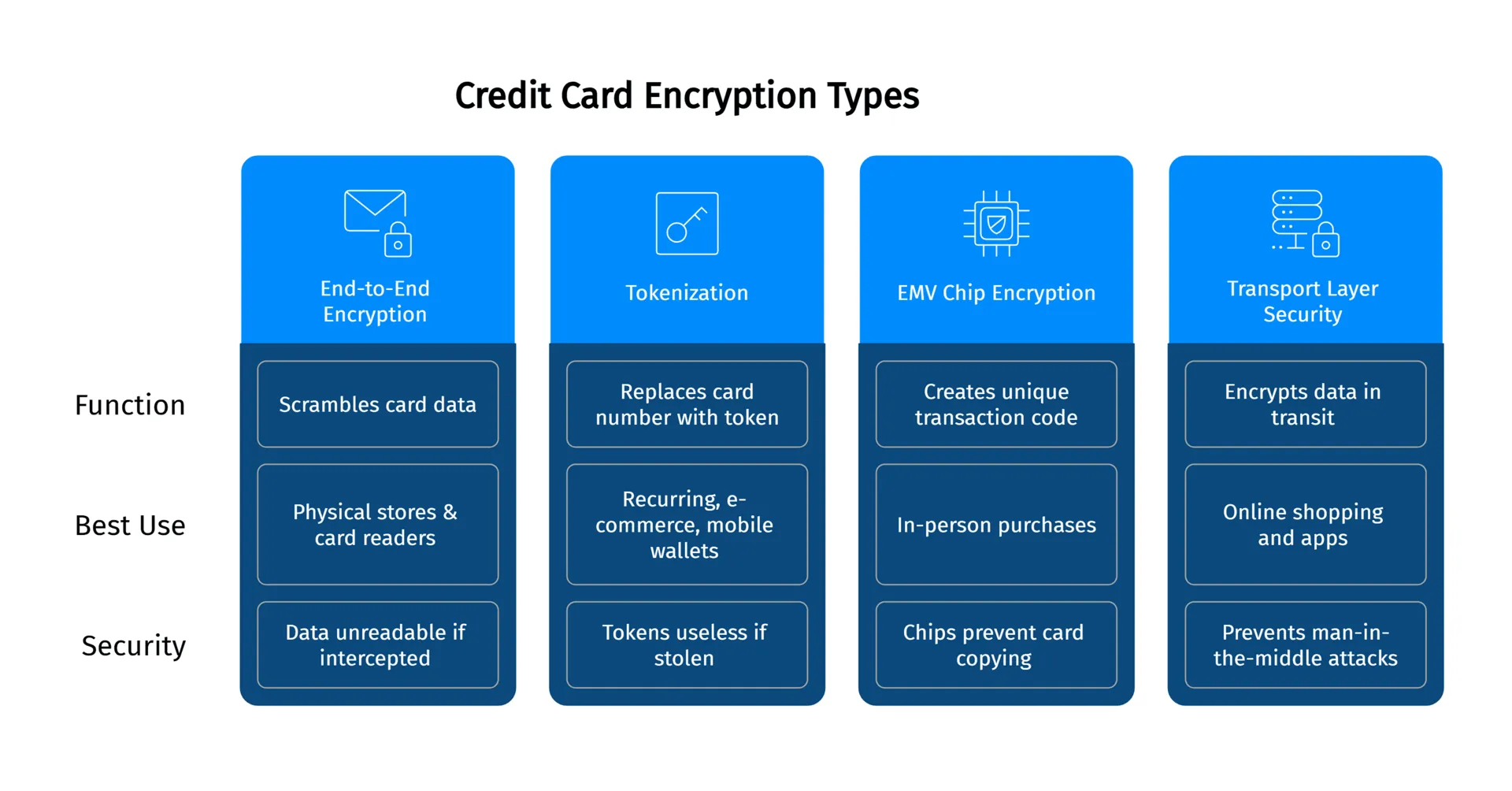

Types of Credit Card Encryption

Credit card encryption comes in different forms, each designed to protect your data at various stages of a transaction. Here’s a quick breakdown:

- End-to-End Encryption (E2EE)

What it does: Scrambles card data immediately when swiped, dipped, or tapped—and keeps it locked until it reaches the payment processor.

Best for: Physical stores & card readers.

🔒Even if hackers intercept the data mid-transaction, they can’t read it.

- Tokenization

What it does: Replaces your actual card number with a random, one-time code (called a "token") for online/mobile payments.

Best for: Recurring subscriptions, e-commerce, and mobile wallets (like Apple Pay).

🔒Tokens are useless if stolen—merchants never store your real card details.

- EMV Chip Encryption

What it does: The gold chip on your card creates a unique transaction code every time you dip it.

Best for: In-person purchases (retail, restaurants, ATMs).

🔒 Unlike magnetic stripes, chips can’t be copied for counterfeit cards.

- Transport Layer Security (TLS)

What it does: Encrypts data while it’s moving between systems (e.g., from your browser to a store’s checkout).

Best for: Online shopping and apps.

🔒 Prevents "man-in-the-middle" attacks on public Wi-Fi.

Tokenization vs. Encryption: What’s the Difference?

While credit card encryption protects data by encoding it, tokenization replaces credit card information with a unique, one-time-use “token.”

Even if the token is intercepted, it can’t be reused or traced back to the cardholder.

Tokenization is especially useful for:

- Mobile wallets (like Apple Pay)

- Recurring or subscription billing

- Online and contactless payments

For high-risk businesses, combining encryption and tokenization is a smart move — it adds multiple layers of protection to reduce fraud and secure customer trust.

Which One Wins?

✅ For physical cards: EMV + E2EE

✅ For online/mobile: Tokenization + TLS

✅ High-risk businesses? Combine all four with fraud tools (like FirmEU’s solutions).

We can help, if you are running a business in a high-risk industry and require a payment processor.

Do Debit Cards Have EMV Chips?

Yes, debit cards, like credit cards, can have EMV chips. This makes both types of cards more secure by generating unique codes for each transaction.

Are Contactless Payments Secure?

Yes, contactless payments, where you simply tap your card on the payment terminal, also rely on EMV chip technology to secure your transaction data. The encryption used ensures that even though you don’t insert your card, the payment is still protected.

Why Cards Still Have Both Chips AND Stripes (For Now)

The Short Answer:

While EMV chips are the global security standard, magnetic stripes remain as a backup for merchants with older systems—especially in the U.S.

Key Details:

- Cost Barrier: Upgrading to EMV terminals averages $2,000 per reader (National Retail Federation).

- Deadline Coming: Mastercard will stop issuing stripe-only cards by 2029.

Key Security Features for High-Risk Industries

Here are some essential security features that high-risk businesses should consider when choosing a payment processor:

- Real-time Fraud Scoring

- What it does: Analyzes every transaction in real-time to detect potentially fraudulent activity before it becomes a problem.

- Why it matters: It helps businesses reduce the risk of chargebacks and avoid reputational damage from fraud.

- What it does: Analyzes every transaction in real-time to detect potentially fraudulent activity before it becomes a problem.

- Dynamic Transaction Routing

- What it does: Routes payments through multiple secure channels to ensure faster, more reliable, and safer transactions.

- Why it matters: By optimizing payment success rates, businesses reduce the likelihood of fraud.

- What it does: Routes payments through multiple secure channels to ensure faster, more reliable, and safer transactions.

- Tokenization

- What it does: Converts sensitive card details into a unique token, which cannot be used by fraudsters even if intercepted.

- Why it matters: Tokenization ensures that businesses never store actual credit card numbers, reducing the risk of data breaches.

- What it does: Converts sensitive card details into a unique token, which cannot be used by fraudsters even if intercepted.

- End-to-End Encryption (E2EE)

- What it does: Ensures that sensitive data is encrypted from the moment it’s entered until it reaches the payment processor.

- Why it matters: E2EE is crucial for in-person and online transactions, as it safeguards sensitive customer information from being accessed by unauthorized parties.

- What it does: Ensures that sensitive data is encrypted from the moment it’s entered until it reaches the payment processor.

- PCI DSS Compliance

- What it does: Ensures that businesses meet the Payment Card Industry Data Security Standard (PCI DSS) to protect cardholder data.

- Why it matters: Compliance helps avoid hefty fines and penalties while building customer trust by showing commitment to data protection.

- What it does: Ensures that businesses meet the Payment Card Industry Data Security Standard (PCI DSS) to protect cardholder data.

Why Encryption Matters for High-Risk Businesses

High-risk industries (like adult entertainment, crypto, and gambling) face 3-5x more fraud attempts than traditional businesses.

Without robust encryption, they face significant consequences:

- Chargebacks skyrocket (costing you $$$ in fees + lost inventory)

- Data breaches trigger fines (up to $100k/month for PCI DSS violations)

- Banks shut down accounts (for "excessive fraud risk")

Incorporating Multiple Security Layers

Encryption is just one part of the equation.

For high-risk businesses, it is crucial to combine encryption with additional fraud prevention mechanisms.

Conclusion: Strengthening High-Risk Business Payment Security

In high-risk industries like adult entertainment, crypto, and gambling, securing sensitive payment data isn't just important-it's essential.

Credit card encryption forms the bedrock of protection, but additional fraud protection tools and compliant payment processing solutions are needed for the unique challenges these industries face.

At FirmEU, we combine military-grade encryption with high-risk-specific safeguards that enhance security for online transactions, reduce fraud, and help businesses maintain compliance with industry regulations.

💡 Pro Tip: Pair EMV adoption with FirmEU’s high-risk payment solutions to future-proof your security.

FirmEU’s solutions provide:

- Real-time fraud detection and scoring.

- Dynamic transaction routing to minimize fraud risks.

- Tokenization and PCI DSS compliance to ensure secure data storage and processing.

By integrating these measures into your payment system, we ensure enhanced protection, reduced fraud, and compliance with industry regulations.

Ready to enhance your payment security?

Contact FirmEU today and see how we can help your high-risk business thrive with our secure, compliant payment processing solutions.

FAQs

No. FirmEU is not a bank or financial institution. We operate as an independent matchmaking platform, connecting businesses with verified financial partners. All onboarding, KYC, and approval decisions are handled directly by the financial institution.

Still Have Questions?

Our sales team would be more than happy to assist with any futher inquiries

Contact Us

International Payment Solutions

Find the Right Banking and Payment Processing Partner for Your Business

Tell us about your company, and we’ll match you with the most suitable global banking or payment providers from our verified network.

Get Matched