High-Risk vs Low-Risk Business: Key Differences

Roan Dollmann

April 14, 2025

1

minutes

Risk classification can seriously impact how your business runs. When one company pays twice the fees and waits weeks longer for payment approvals than its competitor, something's clearly at play – and that something is risk classification.

We’ve seen so many businesses hit roadblocks because they didn’t understand their risk profile. Whether you’re running a well-established company or starting something new, knowing if you’re labeled high-risk or low-risk can make a big difference in how you plan your finances and grow.

In this guide, we’ll break it all down: what makes a business high-risk or low-risk, which industries fall into each category, and how this impacts your day-to-day operations and bottom line.

What Makes a Business High-Risk vs Low-Risk?

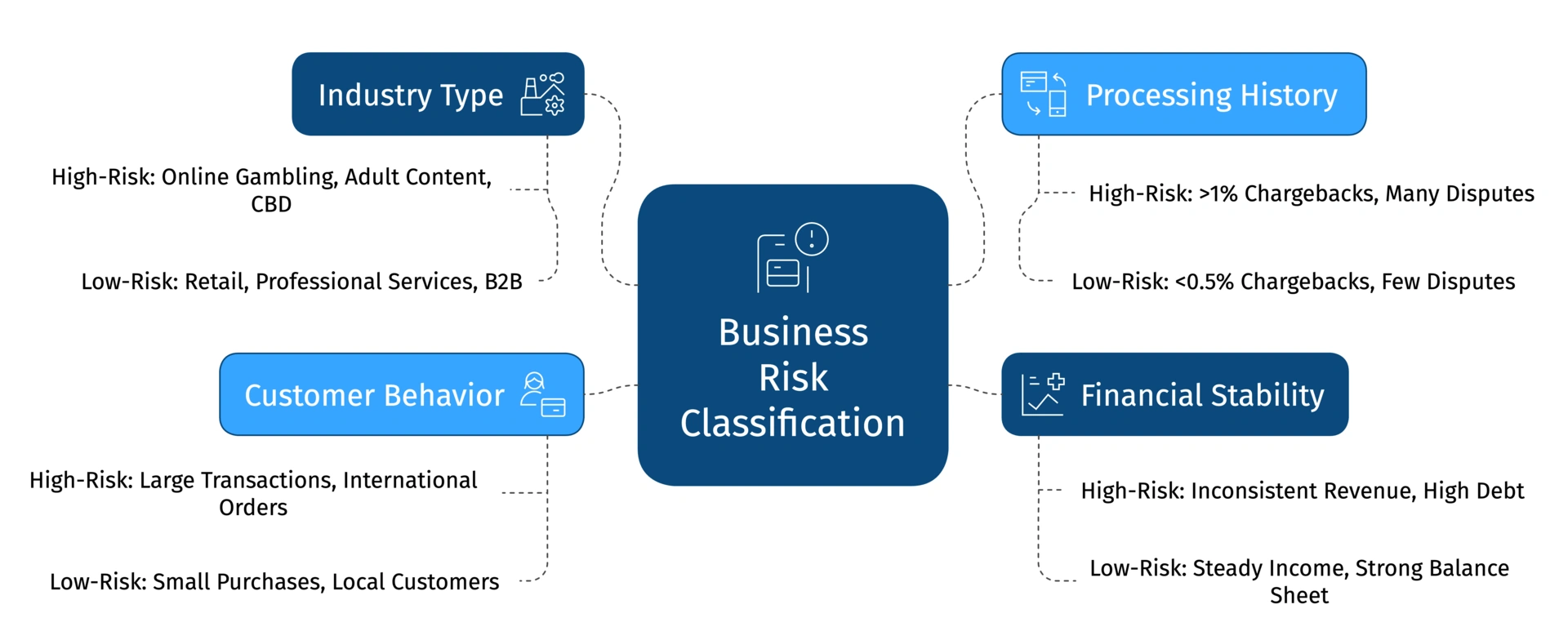

Financial institutions don't classify businesses on a whim. They look at specific factors that have proven reliable predictors of potential problems down the road.

Industry type is the first big factor. Banks and payment processors have "lists" of businesses they consider inherently risky based on historical data. But that's not the whole story.

Your processing history matters tremendously. A track record of:

- High chargeback rates (above 1%)

- Transaction disputes

- Fraud cases

- Payment reversals

...will quickly land you in the high-risk category regardless of your industry.

Financial stability rounds out the picture. A business with healthy cash reserves, steady revenue, and a good credit history typically enjoys a lower-risk classification. Banks and payment processors love predictability – and stable businesses deliver just that.

Customer behavior also factors into your risk assessment. Unusual purchase patterns, strange geographic distribution of orders, or sudden spikes in transaction size can all trigger risk alerts, even for legitimate businesses.

Beyond these factors, high-risk merchant accounts have to deal with extra regulatory hurdles. While all businesses have rules to follow, high-risk companies deal with more frequent audits and detailed reporting requirements.

Industries that fall into the high-risk category

Some industries automatically trigger the high-risk label regardless of how well they're run. These high-risk industries typically include:

- Online gambling and betting platforms – Due to regulatory complexity and fraud potential

- Adult entertainment and content services – Banks view these as reputation risks

- Cryptocurrency businesses – Regulatory uncertainty makes banks nervous

- Travel services – High ticket prices and advance booking create chargeback risks

- Subscription businesses – Recurring billing models face higher dispute rates

- CBD and nutraceuticals – Regulatory gray areas concern financial institutions

A deep understanding of the unique challenges these industries face—whether in payment processing, compliance, or financial operations—is essential to meeting their specific needs. This is something we take great pride in.

Is Your Business Labeled "High-Risk"?

FirmEU specializes in payment solutions for businesses that other processors turn away.

Businesses that typically stay low-risk

Low-risk businesses enjoy smoother financial relationships and fewer processing headaches. These typically include:

- Traditional retail with physical locations

- Professional services like law firms, accountants, and consultants

- Established B2B companies with stable client bases

- Essential services with consistent demand patterns

- Companies with low average transaction values

These businesses enjoy steady revenue, fewer chargebacks, and clearer regulations. For them, payment processing is more of a smooth, behind-the-scenes process rather than a constant challenge.

How High-Risk vs Low-Risk Businesses Operate Differently

Once you understand your risk classification, you'll quickly realize it affects almost everything about how you run your business. The differences go way beyond just higher fees.

Banking relationships look completely different across the risk spectrum. While low-risk businesses might maintain a single banking relationship for years, high-risk companies often maintain relationships with multiple financial institutions as a safety net. They know from experience that account freezes or sudden terminations can happen with minimal warning.

Documentation requirements show another clear contrast. While low-risk businesses fill out basic forms, high-risk operations often prepare thick document packages, including:

.webp)

The weight of compliance requirements falls much heavier on high-risk operations. They invest in strong systems to monitor transactions, prevent fraud, and generate the reports required by regulatory authorities. This often means hiring dedicated compliance staff and implementing specialized technology that low-risk businesses simply don't need.

Improving security measures becomes a daily priority for high-risk operations, requiring ongoing attention rather than the set-it-and-forget-it approach that works for lower-risk companies.

Financial planning also takes different paths. High-risk businesses build big buffers into their cash flow plans, accounting for:

- Higher processing fees

- Rolling reserves held by payment processors

- Potential chargeback losses

- Compliance-related expenses

Low-risk businesses can operate with leaner financial models and more predictable cash flows, giving them more flexibility to invest and expand.

Finding the right payment processing solution

The payment processing world also looks completely different depending on which side of the risk divide you fall. High-risk businesses need specialized solutions with capabilities that standard processors simply don't offer.

High-risk merchants require payment gateways that provide:

- Advanced fraud detection systems

- Customizable security filters

- Multiple processing options for backup

- Strong chargeback management tools

- Multi-currency support

High-risk payment solutions must also address rolling reserves – a critical factor absent from low-risk processing. These reserves typically hold 5-15% of your transaction values for 180 days as a security buffer.

Is Your Business Labeled "High-Risk"?

FirmEU specializes in payment solutions for businesses that other processors turn away.

Customer verification: What you need to know

Know Your Customer (KYC) and Anti-Money Laundering (AML) requirements create another operational divide between risk categories. High-risk businesses use far more thorough verification procedures.

Recent data shows that 90% of financial institutions now use AI and machine learning for AML (Anti-Money Laundering) activities, technology that high-risk businesses must increasingly adopt as well.

.webp)

These verification requirements directly shape the customer journey. High-risk businesses face the challenge of implementing strong security without creating so much friction that legitimate customers abandon their purchases.

High-Risk vs Low-Risk Business: Comparing Costs

Let's talk money – because the financial impact of your risk classification can be substantial. When we look at the numbers, high-risk businesses face significantly higher costs across the board.

Processing fees tell the clearest story:

- Low-risk businesses: Typically pay 1.5% to 2% per transaction

- High-risk businesses: Often charged 3% to 4.5% per transaction

That difference might not seem huge at first glance, but let's put it in perspective. For a business processing $100,000 monthly, that's an extra $2,000+ in fees every month – money that comes straight out of your profit margins.

Beyond the direct fees, high-risk businesses face significant "hidden" costs that don't show up in your processor's rate sheet. High-risk payment gateway fees often include:

- Monthly gateway fees

- Setup fees

- Early termination fees

- PCI compliance fees

- Statement fees

The approval process also costs you time and resources.

Low-risk businesses often receive approval within 24 hours with minimal paperwork. High-risk merchants? You're often looking at 1-2 weeks of underwriting, document collection, and review before you can start processing payments.

High-risk payment processing costs also create an ongoing challenge that affects pricing strategy, profit margins, and cash flow planning. These higher expenses often force businesses to choose between raising prices (risking competitiveness) or accepting lower margins.

Payment Solutions for High-Risk vs Low-Risk Businesses

Now that we understand the cost differences, let's look at the payment solutions themselves. The technology that powers payments for high-risk vs. low-risk businesses differs significantly.

What's fascinating is how payment technology has evolved to address specific risk challenges. PayFirmly reflects this evolution – we've built features specifically designed to handle the complexities high-risk businesses face daily.

Low-risk businesses can typically use standardized solutions with minimal customization. High-risk merchants need systems with much greater flexibility and security capabilities.

The technology differences include:

- Fraud detection capabilities: High-risk systems use advanced AI and machine learning to spot potential fraud, while low-risk solutions can rely on basic rule sets

- Transaction routing: High-risk gateways need intelligent routing to optimize approval rates across multiple processors

- Payment options: High-risk businesses benefit from offering diverse payment methods including crypto payment solutions to reduce dependency on traditional processors

- Integration complexity: High-risk solutions require deeper integration with business systems for better risk management

The processing speed also varies dramatically.

Low-risk transactions typically clear in 1-2 business days. High-risk merchants often have to wait 3-7 days for funds to become available.

What to look for in a high-risk payment provider

If you're operating a high-risk business, choosing the right payment provider becomes critical to your success. So look for these key features:

- Multiple processing relationships – Never depend on a single processor

- Customizable fraud filters that you can adjust based on your specific risk patterns

- Chargeback prevention tools that flag high-risk transactions before approval

- Detailed reporting for tracking transaction patterns and identifying issues

- Advanced security features for high-risk payments like 3D Secure 2.0

The result? Higher approval rates, lower costs, and fewer processing headaches.

Payment solutions when you're low-risk

Low-risk businesses have it easier when it comes to payment processing. Your payment setup will typically be simpler, less expensive, and quicker to implement.

Most low-risk businesses can use standard payment providers with:

- Simple approval processes

- Quick setup (often same-day)

- Straightforward pricing models

- Easy integration with popular platforms

These solutions typically integrate seamlessly with common e-commerce platforms like Shopify, WooCommerce, and Magento without requiring custom development. Setup is often as simple as creating an account, connecting to your platform of choice, and starting to accept payments.

Low-risk businesses rarely need the advanced routing and fraud prevention tools that high-risk merchants depend on. This simplicity translates to lower costs and fewer operational headaches – one of the major benefits of maintaining low-risk status.

High-Risk vs Low-Risk Business: How Regulations Differ

Regulation creates perhaps the starkest contrast between high-risk and low-risk business operations. The regulatory landscape you'll navigate depends heavily on your risk classification.

High-risk businesses face a regulatory burden that can feel overwhelming at times. You're subject to more frequent audits, more detailed reporting requirements, and stricter interpretations of existing regulations. This isn't arbitrary – industries classified as high-risk often have greater potential for financial crimes or consumer harm, prompting closer regulatory attention.

The regulatory differences play out in several key areas:

Documentation requirements:

- Low-risk: Standard KYC documentation, occasional updates

- High-risk: Enhanced due diligence, frequent documentation reviews, ongoing monitoring

Reporting obligations:

- Low-risk: Standard transaction reporting, typically aggregated

- High-risk: Detailed transaction reporting, suspicious activity reporting, regular compliance certifications

Audit frequency:

- Low-risk: Occasional, often triggered by specific events

- High-risk: Regular scheduled audits plus random checks

Compliance requirements scale directly with the risk level.

According to our research, businesses with higher risk profiles face significantly more stringent regulatory oversight and more extensive compliance obligations. The concept of risk-based compliance is becoming standard practice in regulatory frameworks, with authorities focusing more attention on high-risk entities.

Besides that, jurisdictional differences in regulations add additional layer of complexity for high-risk businesses operating internationally. What's permitted in one region may trigger red flags in another, requiring sophisticated compliance strategies for companies with global operations.

Making Risk Work for Your Business

Understanding where your business falls on the risk spectrum – and what that means for your operations – is crucial for planning and success. The differences between high-risk and low-risk businesses touch everything from your day-to-day operations to your long-term growth potential.

Risk classification isn't about "good" versus "bad" businesses.

It's simply a framework financial institutions use to manage their exposure. Plenty of legitimate, successful companies operate in high-risk categories – they just need the right strategies and partners to navigate the challenges.

The key takeaways from our exploration:

- High-risk businesses face higher costs, more complex operations, and greater regulatory scrutiny

- The right payment processing solution can make a dramatic difference in approval rates and fees

- Risk classification impacts everything from banking relationships to customer experience

- With proper planning and the right partners, businesses in any risk category can thrive

At FirmEU, we've guided businesses through risk-classification challenges for years—watching them grow despite (and sometimes because of) their unique position.

Whether you're a low-risk e-commerce looking to streamline your payment process or a high-risk enterprise needing specialized payment solutions, we have walked the path with businesses just like yours. We've seen what works and what doesn't across the risk spectrum.

So ask yourself:

Are you letting your risk classification limit your business, or are you using specialized knowledge to turn it into an advantage? The choice – and the potential – is yours.

Is Your Business Labeled "High-Risk"?

FirmEU specializes in payment solutions for businesses that other processors turn away.

FAQs

No. FirmEU is not a bank or financial institution. We operate as an independent matchmaking platform, connecting businesses with verified financial partners. All onboarding, KYC, and approval decisions are handled directly by the financial institution.

Still Have Questions?

Our sales team would be more than happy to assist with any futher inquiries

Contact Us

International Payment Solutions

Find the Right Banking and Payment Processing Partner for Your Business

Tell us about your company, and we’ll match you with the most suitable global banking or payment providers from our verified network.

Get Matched