Why Cross-Border Payments Take So Long: The Step-by-Step Journey Explained

Garry

April 6, 2026

1

minutes

.webp)

If you’ve ever sent or received an international payment, you already know one thing — it rarely moves as fast as expected. On the surface, everything looks digital and instant. You click “send,” and it feels like the money should reach the other side within seconds. But in reality, cross-border payments still take 1 to 5 business days, and in some cases, even longer. These cross-border payment delays and international payment delays are among the most common challenges businesses face when moving money globally.

It's worth being clear upfront about what this article covers. A payment that's simply slow — still processing, still moving through the system — is a different situation from a payment that's outright rejected or bounced back. If your transaction has actually failed rather than just taken longer than expected, that points to a different root cause, usually something fixable in how the payment was set up. We cover those specific causes and a practical fix framework separately in Why Cross-Border Payments Fail.

From my experience working with global businesses, the biggest confusion is this: “If everything is online, why is it still slow?”

The answer is simple — what you see is just the front end. Behind every international transaction, there’s a multi-layered system, which is better known through understanding how payment processing works involving banks, payment processors, compliance checks, currency conversions, and regional regulations.

In fact, most delays don’t happen because something is “wrong.”

They happen because:

- multiple institutions are involved in one transaction

- every layer performs its own checks and validations

- different countries operate on different financial systems and timelines

- risk policies vary depending on your business model and transaction behavior

And this is exactly where most businesses struggle.

Understanding the causes of cross-border payment delays is important because many of these issues occur behind the scenes and are often outside the sender's immediate control.

We’ve seen cases where perfectly valid transactions get delayed simply because one intermediary bank flagged it for review, or because the payment route wasn’t optimized for that corridor.

At FirmEU, we work closely with businesses dealing with cross-border payments every day, and one thing is clear: delays are not random — they are structural. The time you understand what’s happening behind the scenes, you can actually predict, reduce and even avoid many of such delays.

Pre Requisites For Businesses Regarding Cross Border Payments

1) Clear and accurate transaction details to avoid compliance flags and processing delays

2) Strong banking or payment partner with global coverage and fewer intermediaries

3) Proper KYC and compliance documentation ready to prevent manual reviews

4) Optimized payment routing based on corridor and currency requirements

5) Awareness of cut-off times, time zones, and banking holidays to plan transfers effectively

Now let's explore it step by step.

Tired of Waiting Days for Cross-Border Payments to Clear?

If your international transactions feel slower than they should, the issue often isn’t the bank — it’s how your payment processing system is structured behind the scenes. Small inefficiencies in routing, compliance, or currency handling can quietly add days to every transfer.

How Cross-Border Payments Actually Function (Step-by-Step Guide)

Whenever I explain something related to cross-border payments to clients, the first thing I clarify is that an international transfer is never a simple one-step process. Even though it looks like a direct transfer on the surface, in reality, it moves through multiple systems before reaching the final recipient.

Let me walk you through how it actually works behind the scenes.

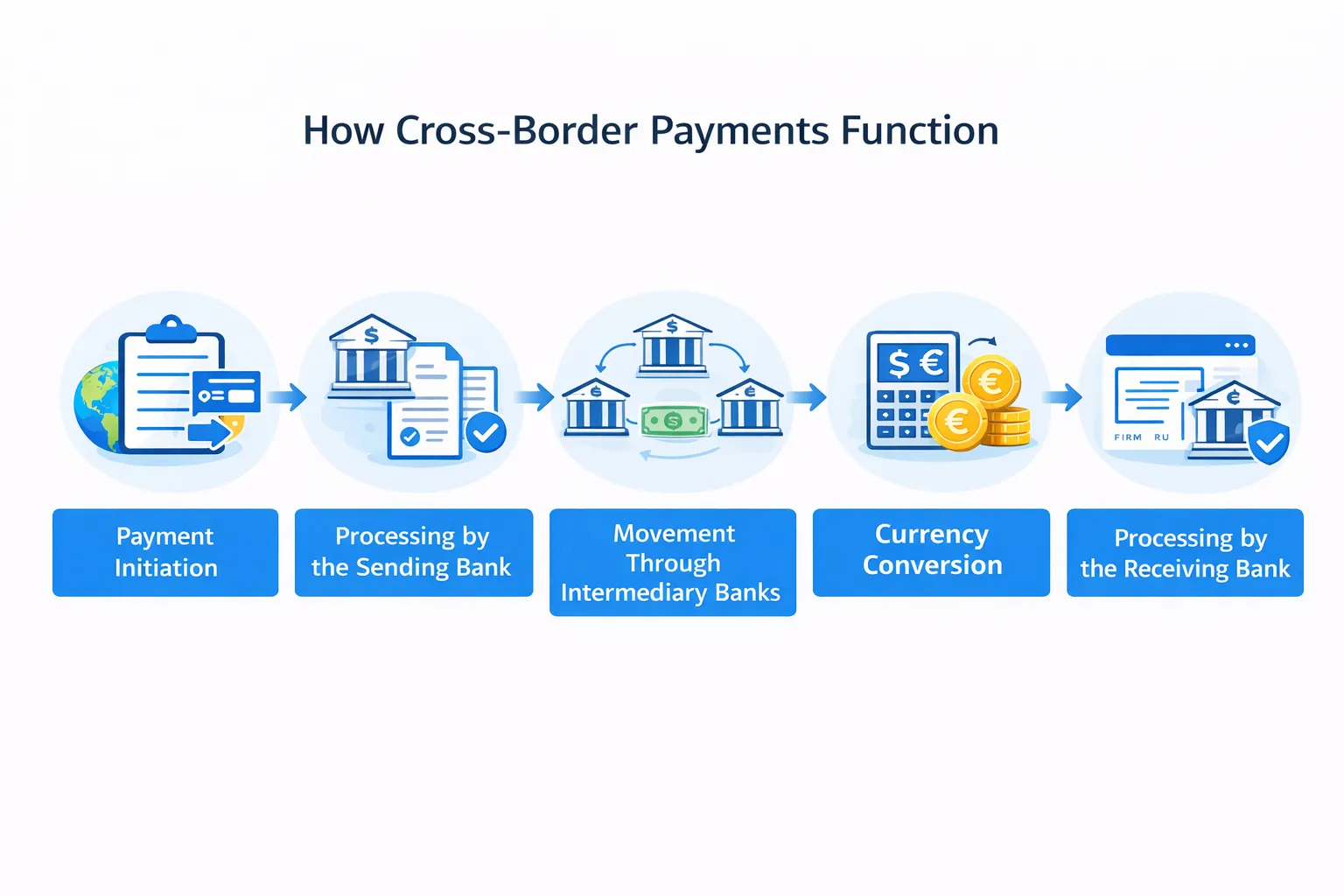

Payment Flow Explained

1. Payment Initiation

The process begins when the sender initiates a transaction through their bank or payment provider. At this point, the system validates basic details such as account information, available balance and transaction format. Everything appears instant here because the request has only just entered the system.

2. Processing by the Sending Bank

Before releasing the funds, the sending bank performs internal checks. These include fraud detection, transaction verification and initial compliance screening. If anything appears unusual, the payment can be temporarily held for review even at this early stage.

3. Movement Through Intermediary Banks

In most cases, the sending bank does not have a direct connection with the receiving bank especially in international transactions. Because of this, the payment is routed through one or more intermediary banks.

Each intermediary acts as a checkpoint. It processes the transaction, may apply its own fees, and runs additional validations. This layer is one of the most common sources of delay because every institution functions with its own rules and processing timelines.

4. Currency Conversion (If Applicable)

If the transaction includes different currencies then conversion takes place somewhere along the route. Depending on the setup, this can happen at the sending bank, an intermediary or the receiving bank.

Currency conversion introduces additional complexity, especially without multi-currency payment processing benefits. Rate confirmation, liquidity availability and timing can all influence how quickly this step is completed.

5. Compliance and Regulatory Screening

At multiple stages, the transaction is checked against regulatory requirements. This includes anti-money laundering checks, sanctions screening, and internal risk assessments.

One important thing many businesses overlook is that these checks are not performed just once. Each institution involved in the payment may run its own compliance process, which can significantly extend processing time.

6. Processing by the Receiving Bank

Once the payment reaches the destination bank then it goes through another round of verification. The bank confirms account details, reviews compliance requirements and may hold the funds briefly before releasing them.

Where Delays Typically Occur

From practical experience, delays can occur at several points across this flow. The most common ones include intermediary banks, compliance checks, and receiving bank processing.

This means that a single transaction can encounter multiple checkpoints, and even a small delay at any one of them can slow down the entire payment. These cross-border transaction delays are one of the primary reasons businesses experience inconsistent settlement times.

The Role of Intermediary Banks (And Why They Cause Delays)

One of the biggest reasons cross-border payments slow down is something most businesses are not even aware of — intermediary banks.

In simple terms, when your bank does not have a direct connection with the receiving bank then the payment has to pass through one or more third-party banks. These are known as correspondent or intermediary banks and they usually act as connectors between financial institutions across different countries.

From my experience, this is where a large portion of delays actually start.

Many delayed international transfers can be traced back to intermediary banking networks where payments pass through multiple institutions before reaching the final destination.

Why Intermediary Banks Exist

Banks around the world do not maintain direct connections with every other bank globally. Instead, they rely on a network of correspondent relationships.

So when a payment is sent internationally:

- your bank forwards it to a partner bank

- that partner may pass it to another bank

- and eventually, it reaches the destination bank

Each step is necessary because of how global banking infrastructure is structured.

Where the Delay Happens

Every intermediary bank involved in the transaction becomes a checkpoint. And each checkpoint presents and introduces its own processing time.

Here’s what typically happens at each stage:

- the payment is received and queued for processing

- internal checks are performed again

- fees may be deducted

- compliance screening is repeated

- the payment is forwarded to the next institution

Even if each bank takes only a few hours, multiple layers can easily turn into 1–2 extra days of delay.

Lack of Visibility

One of the biggest frustrations businesses face is not just the delay, but the lack of visibility and transparency.

Once the payment leaves the sending bank:

- you often cannot see where it is stuck

- you don’t know which intermediary is holding it

- tracking becomes unclear

This creates uncertainty, especially for businesses handling large volumes or time-sensitive transactions.

Compliance Checks: AML, KYC & Sanctions Screening Delays

One of the most common reasons cross-border payments get delayed is compliance, and in many cases, this is also the least understood part of the process.

Every international payment passes through a series of regulatory checks designed to prevent fraud, money laundering, and sanctioned activity. These reviews are also one of the leading causes of cross-border payment delays, particularly when additional documentation or manual verification is required.

This is particularly relevant when evaluating the causes of payment delays and errors in payroll processing, as payroll transfers often involve recurring international transactions that must pass through the same compliance frameworks.

These checks are not just performed once. Instead, they can happen multiple times as the payment moves through different institutions.

When a transaction is initiated, the sending bank performs its own screening based on internal risk policies. As the payment moves forward, intermediary banks may run additional checks using their own systems and criteria. Finally, the receiving bank conducts another round of validation before crediting the funds. Each institution operates in an independent way which means the same transaction can be reviewed several times before it is completed.

In practice, this layered approach creates delays especially when a transaction triggers a risk flag at any stage. Even if the payment is completely legitimate, it may still be paused for manual review. This typically happens when the transaction amount is still higher than usual. When there is a sudden change in payment behavior or when the sender or receiver operates in a sector that is considered higher risk.

Another factor that often gets overlooked is how sensitive compliance systems are to transaction details. Something as simple as an unclear payment description, inconsistent naming or a mismatch in business activity can lead to additional scrutiny. Once flagged, the payment does not move forward until the review is completed and in some cases the additional documents may be requested.

5. Currency Conversion & FX Processing Bottlenecks

Currency conversion is another layer where cross-border payments quietly slow down. For businesses handling payroll across multiple countries, these bottlenecks can contribute to payment delays and errors in multi-currency international payroll transfers, especially when several currencies are involved in a single payment flow.

On the surface, it feels like exchange rates are applied instantly, but in reality, there are multiple decisions and processes happening behind the scenes before the finalization of a conversion.

Where the Conversion Actually Happens

One thing many businesses don’t realize is that currency conversion does not always happen at a fixed point. Depending on the payment route, it can take place at the sending bank, somewhere in between through an intermediary, or at the receiving bank.

Each option has its own processing logic. Some institutions choose to convert early to lock the rate while others delay conversion until the funds reach closer to the destination. This variation alone can impact how quickly a transaction moves forward.

Rate Validation and Liquidity Constraints

Before a conversion is executed, the system needs to confirm the applicable exchange rate and ensure that there is enough liquidity available for that currency pair. This becomes especially important for larger transactions or less common currencies.

In such cases, the provider may not execute the conversion instantly. Instead, it may take additional time to secure pricing or match the liquidity which directly affects the overall payment timeline.

Batch Processing vs Real-Time FX

Not all institutions process foreign exchange in real time. Some banks operate on batch cycles, which is a limitation compared to modern payment localization strategies for international businesses, where conversions are processed at specific intervals during the day.

If a transaction arrives just after a processing window closes, it may have to wait until the next cycle. From the outside, this looks like an unexplained delay even though the payment is technically progressing as per the bank’s internal system.

Multiple Conversions in a Single Transaction

In more complex routes especially those involving intermediary banks, a single payment may go through multiple currency conversions. For example, a transaction might move from one currency to an intermediate currency before reaching the final destination currency.

Each additional conversion introduces another processing step along with potential delays and added costs. This is one of the reasons why some payments feel inconsistent even when the same route is used repeatedly.

Different Banking Systems, Time Zones & Cut-Off Times

Even when everything is working fine technically, cross-border payments can still slow down because global banking does not operate on a single unified system. Each country, each bank, and even each payment rail follows its own timing rules and this creates natural friction in international transactions.

Different Banking Infrastructures Across Countries

Not all banking systems are built the same way. Some regions have highly advanced, near real-time settlement systems while others still rely on traditional batch processing.

When a payment moves from one system to another then it often needs to be adapted or queued according to the receiving system’s rules. This mismatch between infrastructures can create delays even if both sides are functioning correctly within their own frameworks.

Impact of Time Zones on Processing

Time zones play a much bigger role than most businesses expect. A payment initiated during business hours in one country may arrive outside working hours in another one.

In such cases, the transaction simply waits until the receiving institution resumes operations. This becomes even more noticeable when payments move across regions like Asia, Europe, and the US where time zones and differences can stretch processing across multiple calendar days.

Banking Cut-Off Times and Processing Windows

Every bank operates with defined cut-off times for processing payments. If a transaction is submitted before the cut-off then it is processed on the same day. If it misses the window, it is pushed to the next business day.

This is one of the most common yet least visible reasons for delays. It is also among the common reasons for payroll delays international payments multi currency environments where organizations depend on precise payment timing across several regions.

From a user’s perspective, the payment was sent “on time,” but internally, it entered the system just after the processing window closed.

Weekends and Public Holidays

Another factor that often gets overlooked is the difference between holidays and non-working days across countries. A payment may be in progress but if one of the involved institutions is closed due to a local holiday, the transaction pauses until operations resume.

This is why some cross-border payments appear to stall unexpectedly especially when moving across multiple regions with different holiday calendars.

Why Do These Delays Feel Unavoidable?

Unlike compliance or routing issues, these delays are not caused by errors or inefficiencies. They are simply a result of how global banking systems are structured.

However, the impact can still be reduced by choosing the right partners and payment routes. At FirmEU, we help businesses connect with banks and payment providers that offer better alignment in terms of processing windows, regional coverage, and settlement capabilities. This helps in reducing timing mismatches and keep payments moving more consistently.

Conclusion: What Businesses Should Do Differently

Cross-border payment delays are rarely random. From everything we’ve covered, it becomes clear that these delays are built into the system itself. Multiple institutions, layered compliance checks, currency conversions and differences in banking infrastructure all contribute to the international payment processing time required for funds to move from one country to another.

The mistake most businesses make is assuming that delays are unavoidable and cannot be controlled. In reality, while you cannot eliminate every delay but you can significantly reduce them by improving how your payment flow is structured.

From a practical standpoint, this means working with the right mix of banking partners, reducing unnecessary intermediaries. Along with that, aligning with providers that understand your business model and optimizing how your transactions are routed globally.

In my experience, businesses that take this approach to move from unpredictable payment timelines to far more stable and reliable operations. Instead of constantly reacting to delays, they gain better visibility and control over how their funds move across borders.

At FirmEU, this is exactly what we focus on. We help businesses connect with banking and payment partners that are aligned with their structure, geography and transaction patterns. By doing this, we simplify access to global financial infrastructure and reduce the friction that typically slows down cross-border payments.

Fix Your Cross-Border Payment Delays

If your international payments are slow, inconsistent, or getting stuck, the issue is usually in the structure — not the system. At FirmEU, we help businesses streamline payment flows, reduce intermediaries, and build faster, more reliable cross-border setups.

FAQs

What are SWIFT payment delays and why do they happen?

SWIFT payment delays explained simply come down to the number of institutions involved in the transaction. Because SWIFT payments often move through intermediary banks, each institution may perform its own compliance and verification checks, which can increase processing times.

How can businesses reduce cross-border payment fees along with delays?

By minimizing intermediary banks, choosing the right payment corridors and using providers with transparent FX pricing.

Are there faster alternatives to traditional bank transfers for international payments?

Yes, fintech platforms, local payment rails, and real-time networks can significantly reduce transfer time compared to SWIFT-based transfers.

Does the size of a transaction impact processing time?

Yes, higher-value transactions are more likely to trigger additional compliance checks which can lead to longer processing times.

How do business industries affect cross-border payment speed?

Certain industries considered high-risk (like crypto, gaming, or adult) often face stricter compliance checks that might lead to more frequent delays.

No. FirmEU is not a bank or financial institution. We operate as an independent matchmaking platform, connecting businesses with verified financial partners. All onboarding, KYC, and approval decisions are handled directly by the financial institution.

Still Have Questions?

Our sales team would be more than happy to assist with any futher inquiries

Contact Us

International Payment Solutions

Find the Right Banking and Payment Processing Partner for Your Business

Tell us about your company, and we’ll match you with the most suitable global banking or payment providers from our verified network.

Get Matched