BNPL 2.0: How Buy Now, Pay Later is Expanding Beyond Retail

Roan Dollman

September 12, 2025

1

minutes

Buy Now, Pay Later (BNPL) changed how consumers shop – but now, it’s evolving.

Welcome to BNPL 2.0: a smarter, broader, and more credit-aware generation of installment finance.

We’re witnessing BNPL step outside the e-commerce checkout and into everything from healthcare and travel to professional services and education. For consumers, it’s flexibility. For businesses, it’s a powerful new growth lever.

In this guide, we’ll explore:

- What BNPL 2.0 actually means

- How it differs from traditional BNPL

- Which industries are adopting it

- Its impact on credit scores

- The risks and business considerations

Let’s dive in.

What is BNPL 2.0 and How is It Different from Traditional BNPL?

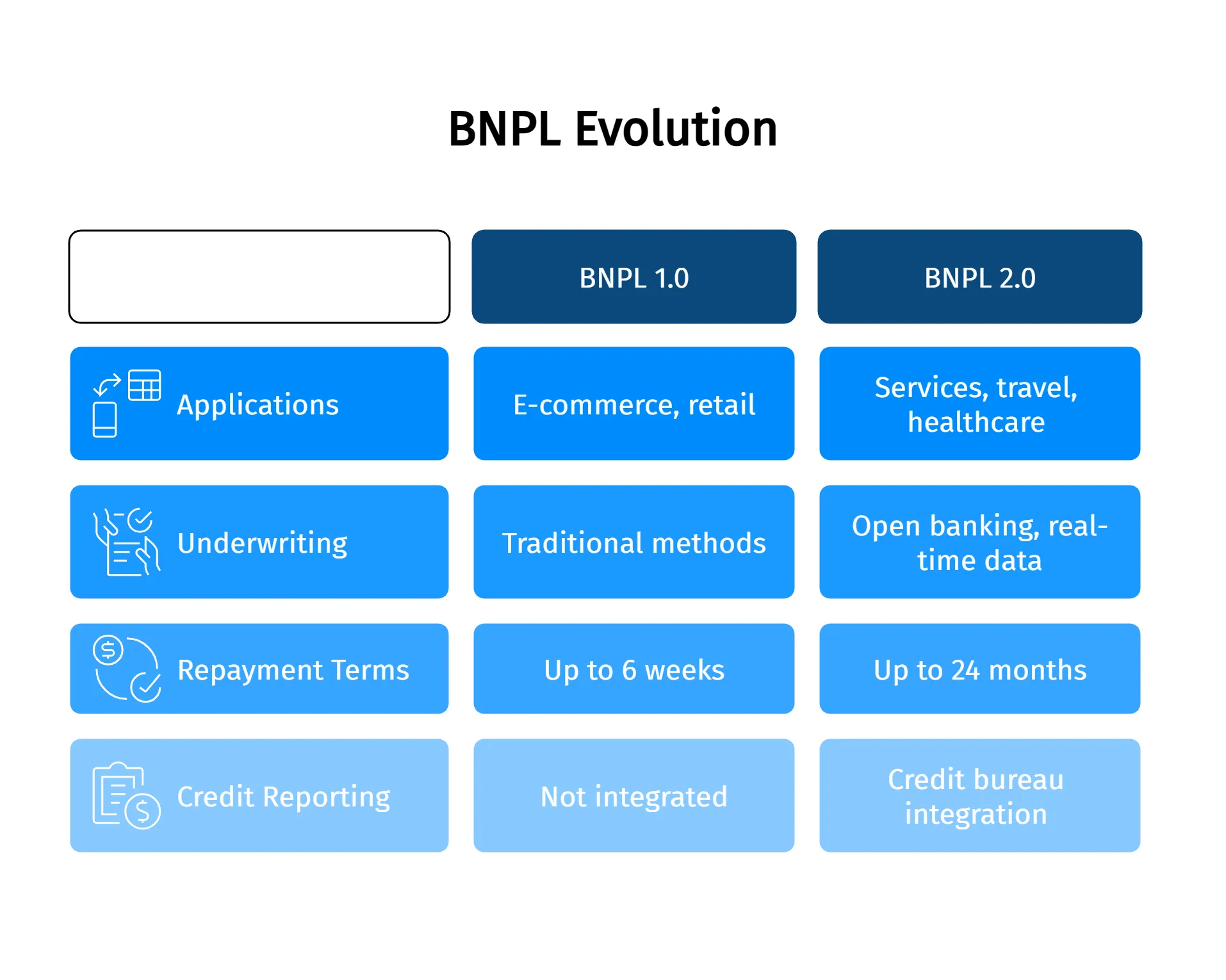

BNPL 2.0 represents the next phase in Buy Now, Pay Later services – more regulated, more sophisticated, and far more integrated across industries.

BNPL 2.0 is not just a payment method – it’s a financial product. It supports responsible credit usage, connects with traditional finance infrastructure, and unlocks access to services that previously required upfront payment.

BNPL 1.0 was about speed. BNPL 2.0 is about stability, access, and growth.

Learn more about high-risk business financing in our latest guide.

Which Industries Are Adopting BNPL 2.0 Beyond Retail?

BNPL 2.0 is being adopted rapidly in sectors where affordability is a barrier and flexibility creates opportunity.

In healthcare, patients are using BNPL to finance elective procedures like cosmetic and dental treatments. Mental health platforms such as Talkspace have integrated pay-later options for therapy sessions, while prescription and diagnostic services are embracing flexible installment plans to improve accessibility.

In the travel sector, BNPL 2.0 makes vacationing more attainable. Consumers can now split payments for flights, hotels, and cruise packages over time. Platforms like Amadeus have partnered with BNPL providers like Klarna to offer these plans directly at checkout.

Ready to Offer BNPL 2.0 the Right Way?

Get strategic support for BNPL partner selection, integration, and growth tracking.

Education has become one of the fastest-growing verticals. From online certifications through Coursera and edX to tech bootcamps and microdegree programs, BNPL is helping learners access skills-based programs without large upfront costs. Even language courses and tutoring services are now BNPL-enabled.

For professional services, clients can spread payments for legal retainers, tax advisory packages, and freelance service bundles. This makes high-cost expertise more affordable to small businesses and solopreneurs.

Even the automotive industry is joining in. From repairs and servicing to car subscriptions and aftermarket upgrades, installment payment plans are gaining popularity.

How Does BNPL 2.0 Impact Consumer Credit Scores?

One of the biggest shifts in BNPL 2.0 is its role in credit visibility. Unlike early BNPL systems, which had minimal credit impact, BNPL 2.0 platforms actively report to major bureaus.

BNPL 2.0 platforms now report to bureaus like Equifax, Experian, and TransUnion. This helps build credit for responsible users and increases transparency across financial systems.

But it also raises the stakes – missed payments now carry real-world consequences.

Are There Any Risks Associated with BNPL 2.0 for Businesses?

Yes. While the potential upside is huge, BNPL 2.0 isn’t risk-free for merchants or service providers.

Key business risks include:

- Customer defaults: Even with third-party BNPL, poor repayment can affect merchant settlements

- Increased regulation: BNPL is now considered a credit product in Australia, the UK, and parts of the EU

- Operational complexity: Refunds, chargebacks, and dispute handling with installments require process updates

Risk mitigation strategies:

- Work with regulated BNPL providers that offer strong underwriting and fraud detection

- Ensure clear UX messaging about repayment terms

- Monitor performance dashboards monthly for conversion vs. delinquency insights

What Should Businesses Consider Before Offering BNPL 2.0?

Before integrating BNPL 2.0 into your payment stack, ask:

Product & Audience Fit

- Does your product have a mid-to-high price point?

- Does your customer base (Gen Z, freelancers, underbanked) demand payment flexibility?

Operational Readiness

- Are you prepared for BNPL fees and cash flow delays?

- Can you handle edge cases like partial refunds or abandoned plans?

Technical Integration

- Do you have the platform (Shopify, Stripe, custom CMS) to support plug-and-play BNPL?

- Are your analytics tools ready to measure BNPL-driven conversion?

Compliance Requirements

- Are you operating in regulated markets?

- Have you assessed GDPR, PCI, and PSD2 implications?

The BNPL 2.0 Revolution Is Already Underway

BNPL 2.0 is no longer theory – it’s being embedded into how people live:

- 25% of U.S. consumers used BNPL for groceries in 2025

- 60% of Coachella attendees financed tickets via BNPL

- Providers like Affirm, Zip, and Sezzle now offer debit cards, cashback, and savings tools

BNPL 2.0 is becoming a complete financial ecosystem – offering payment, credit building, and budgeting tools in one.

The Future of Flexible Finance

BNPL 2.0 is more than a payment trend – it’s a new way for people to access what they need, when they need it.

From mental health support to career upskilling and travel experiences, BNPL 2.0 brings affordability and dignity back into modern finance.

For businesses, it’s an opportunity to improve conversion, retention, and lifetime value – while also building deeper customer relationships.

At FirmEU, we help businesses:

- Vet compliant BNPL 2.0 partners

- Integrate with best-in-class platforms

- Monitor performance and optimize growth

Ready to Offer BNPL 2.0 the Right Way?

Get strategic support for BNPL partner selection, integration, and growth tracking.

FAQs

No. FirmEU is not a bank or financial institution. We operate as an independent matchmaking platform, connecting businesses with verified financial partners. All onboarding, KYC, and approval decisions are handled directly by the financial institution.

Still Have Questions?

Our sales team would be more than happy to assist with any futher inquiries

Contact Us

International Payment Solutions

Find the Right Banking and Payment Processing Partner for Your Business

Tell us about your company, and we’ll match you with the most suitable global banking or payment providers from our verified network.

Get Matched