SEPA Europe: How It Works for EU and Non-EU Companies

Roan Dollmann

September 18, 2025

1

minutes

If your business deals with payments across Europe, understanding SEPA (Single Euro Payments Area) is crucial.

This payment network makes cross-border transactions within Europe as simple and cost-effective as domestic transfers.

Whether you're an EU-based company or expanding into Europe from abroad, SEPA can significantly improve your payment efficiency.

In this guide, we'll explain how SEPA Europe works, which countries are included, and how businesses, especially in high-risk sectors like gaming, crypto and e-commerce can leverage it for smoother financial operations.

Plus, discover how FirmEU helps companies access SEPA payment solutions, even when traditional banking isn't an option.

What is The SEPA Zone in Europe?

SEPA Europe refers to the Single Euro Payments Area, a unified payment network that enables fast, low-cost, and standardized euro transactions across European countries.

Created by the European Union, SEPA was designed to simplify cross-border EU bank payments, making them as easy as local transfers within a single country.

Within this zone, individuals and businesses can send and receive single euro payments using standardized formats like IBAN (International Bank Account Number) and BIC (Bank Identifier Code) within seconds.

The SEPA zone includes both EU member states and several non-EU countries that have agreed to follow the same payment rules and infrastructure.

The transfer scheme enables transactions to be completed in seconds where supported.

No currency conversion is required, and all transactions can be made easily through online banking, except for countries like Switzerland and the UK that do not use the euro.

The goal of SEPA is to increase efficiency and transparency in European payment systems, benefiting businesses of all sizes - from startups to multinational corporations.

This shared framework improves efficiency, transparency, and reliability in the European payments landscape.

Whether you're based in the EU or operating internationally, having access to SEPA allows you to move money quickly, easily, and affordably across borders.

For companies in high-risk or global industries such as crypto, gaming, forex, or AI, understanding SEPA is especially important.

With the right banking setup, even non-EU companies can benefit from participating in the SEPA payment network.

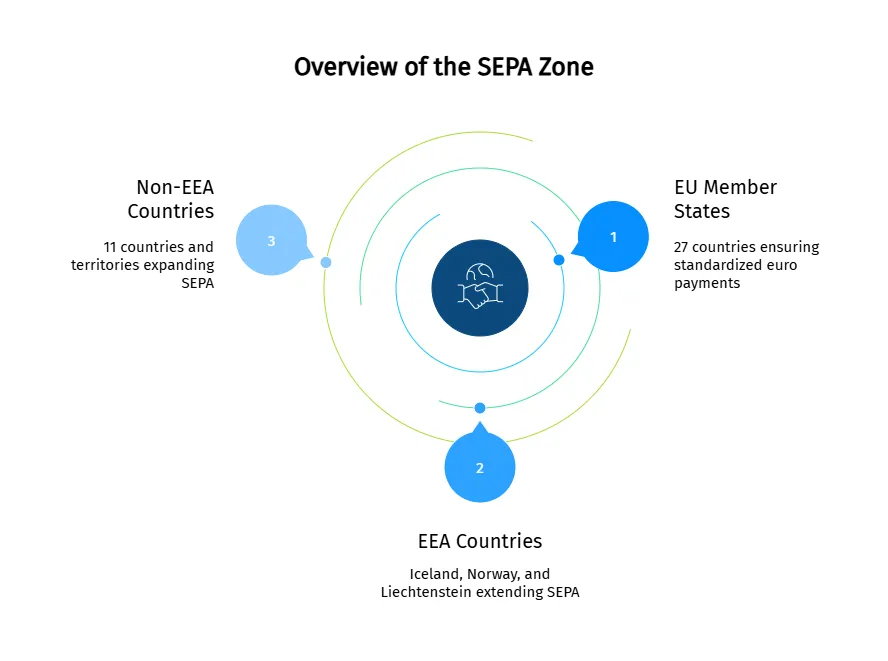

Which Countries are in the SEPA Zone?

The SEPA zone list 2025 helps businesses understand which countries and territories support euro-denominated payments under the SEPA payment network.

Currently, the SEPA zone includes 41 participating countries and territories.

All 27 EU member states are part of SEPA Europe, ensuring full access to standardized single euro payments across the European payment area.

These are:

Austria, Belgium, Bulgaria, Croatia, Cyprus, the Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, the Netherlands, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, and Sweden.

In addition to all 27 EU member states, the SEPA zone includes three countries from the European Economic Area - Iceland, Norway, and Liechtenstein.

It also extends to 11 non-EEA countries and territories that joined after the scope of SEPA was expanded.

These are:

Albania, Andorra, Moldova, Monaco, Montenegro, North Macedonia, San Marino, Serbia, Switzerland, the United Kingdom, and Vatican City.

Together, these jurisdictions make up the European payment area where SEPA rules apply.

For businesses involved in e-commerce, crypto, or other international sectors, being part of, or having access to the SEPA zone is key to simplifying payments across Europe.

This broad participation allows companies with a European SEPA bank account to operate efficiently across borders and access unified European payment systems.

The term "European SEPA bank account" is commonly used but not an official legal or regulatory term. Simply put, it means:

A bank account held in a European financial institution that supports SEPA payment schemes, allowing the account holder to send and receive euro payments across the SEPA zone efficiently and under standardized SEPA rules.

Which Countries are Not Part of the SEPA zone?

Although SEPA covers most of Europe, some areas are not included, such as the Danish Faroe Islands and Greenland.

Kosovo and Montenegro also use the euro as their official currency, but they are not part of the SEPA zone.

Because of this, it’s important for businesses and customers to be aware of which countries are not in SEPA, as different rules and regulations may apply in those places.

Additionally, some countries that use IBAN numbers for bank accounts do not belong to SEPA. Examples include Belarus, Brazil, Saudi Arabia, Turkey, Ukraine, and the United Arab Emirates.

Is the UK in the SEPA zone?

Yes, as mentioned above the United Kingdom remains a member of the SEPA zone even after leaving the EU on February 1, 2021.

Being part of SEPA is not limited to EU members, so UK banks continue to offer euro payment services within SEPA, allowing smooth cross-border transfers across the zone.

Is Switzerland in the SEPA zone?

Yes, Switzerland has been part of the SEPA zone since 2015.

This means Swiss businesses and individuals benefit from faster and simplified cross-border euro payments, including SEPA Credit Transfers and SEPA Direct Debits.

While SEPA transfers to Switzerland are usually free, they may sometimes involve currency conversion fees since Switzerland's currency is the Swiss franc.

What Are the Key SEPA Requirements for EU Companies?

To use SEPA, your company must:

- Have a euro-denominated bank account in an EU country that’s part of SEPA.

- Use the IBAN and BIC format for all payments.

- Comply with local banking rules and SEPA payment regulations.

- Ensure correct customer data (name, IBAN, BIC) to avoid failed transactions.

Can Non-EU Companies Use SEPA?

Yes, non-EU companies can use SEPA payments to send and receive payments across Europe.

However, they cannot join SEPA directly on their own. Instead, they need to work with banks or payment providers that are part of the SEPA network.

To use SEPA, a non-EU business must:

- Have a bank account with a financial institution located in a SEPA-participating country, or

- Use a payment service provider authorized to handle SEPA payments.

This way, even companies based outside Europe can benefit from fast, secure, and low-cost euro transactions within the SEPA zone.

What Are the Key SEPA Requirements for Non-EU Companies?

If you are a non-EU company looking to use SEPA payments, you should know these important requirements:

- European IBAN: You need a bank account with an IBAN from a SEPA country to send or receive SEPA payments.

- SEPA-Compatible Bank: Your bank or payment provider must be part of the SEPA network and support SEPA Credit Transfers (SCT) and/or SEPA Instant Payments (SCT Inst).

- Business Presence (Sometimes Required): Some banks may require proof of a registered EU entity, office, or active business operations in Europe before opening an account.

- Compliance Documents: Expect to provide typical KYC (Know Your Customer) documents, such as company registration certificates, shareholder information, and proof of commercial activities.

- Currency: All SEPA payments must be made in euros. Currency conversion is not handled within SEPA, so operations and invoicing should be in euros.

Finding the right bank or fintech provider experienced with international clients is often the key to accessing SEPA services as a non-EU company.

Get SEPA Access Built for High-Risk Businesses

Whether you're in crypto, gaming, e-commerce, or another high-risk industry, FirmEU helps you set up SEPA-ready accounts and payment solutions that work.

Can non-EU Companies Open a SEPA-Compliant Euro Account Remotely?

Yes, non-EU companies can open a SEPA-compliant euro account remotely, but there are some important points to keep in mind:

- Many banks and payment providers in SEPA countries now offer remote account opening, allowing businesses outside the EU to open euro accounts without being physically present in Europe.

- To open such an account, the bank or payment service provider must be authorized in a SEPA-participating country and comply with SEPA rules and regulations.

- Some non-EU banks have gained direct access to SEPA payment schemes, which makes it easier for their clients to perform SEPA transfers swiftly and securely.

- However, there can be requirements like identity verification, business documentation, and compliance checks that you will need to complete during the remote onboarding process.

- Banks in countries like Switzerland, San Marino, Jersey, and others, which are part of SEPA or linked to it, often facilitate opening euro accounts for international clients remotely.

- Using fintech providers or specialized banking platforms can also simplify the remote opening of SEPA-compliant accounts for non-EU businesses.

What are the Benefits of Using SEPA for Businesses (EU & Non-EU)?

SEPA simplifies European payments, offering clear advantages:

- Cost Savings: Cross-border euro payments are as cheap as local ones, drastically cutting fees.

- Faster Payments: Standard transfers arrive in one day; Instant SEPA takes seconds, 24/7.

- Simpler Operations: Use one standardized system (IBAN/BIC) across 41 countries, reducing errors and admin.

- Easier Expansion: Easily pay and get paid across Europe, boosting your market reach.

- Better Cash Flow: Faster payments and predictable processing improve your financial management.

- High Security: Benefits from strict EU regulations, ensuring safe and fraud-protected transactions.

For Non-EU Companies: Gain easy access to Europe's unified payment system, enabling local payment options for EU customers and stronger competition.

What Are the Different Types of SEPA Payments?

There are three main types of SEPA payments: SEPA Credit Transfer (SCT), SEPA Direct Debit (which includes SDD Core and SDD B2B), and SEPA Instant Credit Transfer (SCT Inst), which let you send money almost right away.

Each serves a different purpose depending on how and when you need to move money.

SEPA Credit Transfer (SCT)

This is the most common type of SEPA payment. It’s used to send money from one euro bank account to another within the SEPA zone.

- Usually takes one business day

- Ideal for paying suppliers, salaries, or invoices

- Only works in euros

- Requires the recipient’s IBAN

SEPA Direct Debit (SDD)

This lets a business or service provider pull money from a customer’s bank account with permission.

- Great for recurring payments like subscriptions or utility bills

- The customer must authorize the payment

- Works only in euros and within the SEPA zone

- Money is collected automatically on the agreed date

SEPA Instant Credit Transfer (SCT Inst)

This is the fastest SEPA payment option. It lets you send money almost immediately, 24/7, even on weekends and holidays.

- Money arrives in seconds

- Works across participating SEPA countries

- Maximum transfer amount is usually up to €100,000 (depending on the bank)

- Great for urgent payments or real-time transfers

In brief:

- Use Credit Transfer for regular payments

- Use Direct Debit for automatic, recurring charges

- Use Instant Transfer for sending money right away

All three are part of the SEPA payment network and make doing business in SEPA Europe faster, easier, and more efficient.

Are SEPA Payments Safe and Regulated?

Yes, SEPA payments are safe and regulated. They follow strict European Union rules designed to protect customers and prevent fraud.

Banks and payment providers in the SEPA system must verify identities, check transactions against sanction lists, and use real-time fraud detection tools.

Since January 2025, SEPA Instant Payments require payments to be completed within 10 seconds, with enhanced security measures in place.

These regulations ensure that euro payments across Europe are fast, secure, and reliable.

What Security and Fraud Prevention Measures are Standard Within SEPA payment?

As discussed, SEPA payments use strong security and fraud prevention measures to keep your money safe. These include:

- Real-time fraud monitoring: Banks and payment providers check transactions instantly to spot and stop suspicious activity before it happens.

- Strong customer authentication: Payments require secure identity checks to confirm who is sending money.

- Sanctions screening: Transactions are regularly screened against EU sanctions lists to block payments involving restricted or risky parties.

- Advanced technologies: Many use AI and machine learning to detect unusual patterns and prevent fraud faster.

- Data protection: Customer information is protected by strict EU rules like GDPR, along with encryption and tokenization.

- User awareness: Tips like verifying emails, avoiding suspicious links, and using two-factor authentication help protect users from scams such as phishing.

SEPA vs SWIFT: What’s the Difference?

SEPA and SWIFT are both international payment systems, but they serve different purposes and operate in different ways.

1. Geographic Coverage

- SEPA: Works only within the SEPA zone.

- SWIFT: Global system covering over 200 countries.

2. Currency

- SEPA: Only supports payments in euros.

- SWIFT: Supports multiple currencies, including USD, GBP, EUR, and more.

3. Speed

- SEPA: Transfers usually take 1 business day, or just seconds with SEPA Instant.

- SWIFT: Transfers take 1–5 business days, depending on the banks and countries involved.

4. Cost

- SEPA: Usually low-cost or even free within the EU. (Some banks may still apply small fees)

- SWIFT: More expensive - fees can be charged by the sender, recipient, and intermediary banks.

5. Use Case

- SEPA: Ideal for euro payments within Europe - fast, cheap, and standardized.

- SWIFT: Best for international, multi-currency transfers outside Europe.

How Does SEPA Support High-Risk Industries Like Crypto and Gaming?

SEPA helps high-risk industries such as cryptocurrency platforms and online gaming companies send and receive euro payments quickly, securely, and following EU regulations.

Key ways SEPA supports these industries:

- Instant and Reliable Payments:

SEPA Instant Credit Transfers (SCT Inst) enable euro payments within seconds, 24/7. This speed is essential for crypto and gaming businesses handling real-time deposits and withdrawals.

- Stronger Compliance and Fraud Prevention:

Banks and payment providers must regularly verify payment recipients and screen transactions against sanction lists.

This reduces risks of fraud and money laundering, which are common in these sectors.

- Aligned with EU Regulations:

SEPA payments comply with major EU rules such as PSD2 and the Funds Transfer Regulation, ensuring strict standards for customer verification and secure money transfers. - Easier Integration for Crypto Companies:

Updated SEPA rules encourage licensed crypto providers to seamlessly work with traditional banks, allowing smooth euro payments within Europe. - Lower Barriers and More Fairness:

SEPA requires transparency and equal fees for instant payments, making it easier for high-risk businesses to access euro payment services fairly.

Can SEPA Payments Be Used for Cryptocurrency Transactions or Exchanges?

Yes, SEPA payments are widely used to fund cryptocurrency exchange accounts or to withdraw euros from them, but with some important points:

- SEPA transfers move euros quickly and securely between bank accounts inside the SEPA zone.

- Most European crypto exchanges accept SEPA payments for deposits and withdrawals, making them a popular euro payment method.

- SEPA payments only handle fiat euros, not cryptocurrencies directly - they transfer funds to/from your bank account, which can then be used on crypto platforms.

- Since 2024–2025, new SEPA regulations require payment providers to include detailed origin-of-funds information for transactions involving crypto, to comply with anti-money laundering (AML) laws.

- Crypto businesses and exchanges must be properly licensed and follow regulations to use SEPA payments smoothly and legally.

Summary:

SEPA’s fast, secure, and regulated euro payments system supports high-risk sectors like crypto and gaming by enabling real-time euro transfers and enforcing strong compliance.

While SEPA itself does not transfer cryptocurrencies, it provides the vital euro payment infrastructure trusted by licensed crypto platforms across Europe.

How Are SEPA Instant Payments Changing Euro Transfers in 2025?

Starting October 5, 2025, SEPA Instant Payments will change euro transfers by making them faster, more secure, and easier to access.

Here’s what will happen:

- Euro payments will be processed and settled in 10 seconds or less, anytime- 24/7, all year round.

- Banks must offer instant payments at the same cost as regular SEPA payments, so sending money won’t cost more just because it’s faster.

- New rules require banks to verify recipient details to prevent fraud but make sanction checks less time-consuming.

- These changes are part of a bigger plan under the EU’s Instant Payments Regulation to modernize and speed up payments across Europe.

In short, from late 2025, sending euro money across Europe will be almost instantaneous, cheaper, and safer - making everyday payments and business transfers much smoother.

Common SEPA Payment Issues and How to Fix Them

SEPA payments are usually reliable, but issues can still happen.

Here are common problems and how to resolve them:

- Incorrect Details: Make sure the IBAN, BIC, and recipient name are accurate. Even small errors can cause payment failures.

- Insufficient Funds: Check that your account has enough balance before sending a payment.

- Instant Payment Not Supported: If SEPA Instant fails, the recipient’s bank may not support it. Your bank may convert it to a standard SEPA Credit Transfer.

- Direct Debit Mandate Problems: Mandate errors or expired authorizations can cause SEPA Direct Debit failures. Confirm the mandate is valid and registered.

- Account Restrictions: If the recipient’s account is blocked, closed, or has limits, contact them for an alternative.

- Compliance Checks: Payments flagged for review may be delayed. Ensure your payment details are clear and legitimate.

- Technical Glitches: Occasional system issues can affect transfers. Try again later or contact your bank.

For any ongoing issues, check your banking platform for error messages or contact your provider for help.

SEPA Europe Solutions for High-Risk and Global Businesses

Need access to SEPA Europe but facing challenges with traditional banks?

FirmEU helps both EU and non-EU companies, including those in high-risk sectors like crypto, gaming, and e-commerce, set up European SEPA bank accounts and access reliable payment solutions.

With deep expertise in international banking, regulatory compliance, and company formation, FirmEU provides tailored guidance to help your business operate confidently across the Single European Payment Area.

We ensure your business can fully benefit from SEPA's efficiencies, allowing you to focus on growth while we handle the complexities of international payments.

Take Control of Your Euro Payments Today

Access SEPA banking solutions tailored to your business needs - no matter your industry or location.

FAQs

No. FirmEU is not a bank or financial institution. We operate as an independent matchmaking platform, connecting businesses with verified financial partners. All onboarding, KYC, and approval decisions are handled directly by the financial institution.

Still Have Questions?

Our sales team would be more than happy to assist with any futher inquiries

Contact Us

International Payment Solutions

Find the Right Banking and Payment Processing Partner for Your Business

Tell us about your company, and we’ll match you with the most suitable global banking or payment providers from our verified network.

Get Matched