How to Accept Payments Globally Without Getting Blocked

Gary

April 29, 2026

1

minutes

Global commerce has made it possible for even small businesses to sell across borders within days. But payments have not evolved at the same pace. While acquiring international customers is easier than ever, getting paid smoothly is where most businesses start facing unexpected friction. Most merchants assume that once they integrate a payment gateway, global payments will “just work.” In reality, that is rarely the case. Transactions get flagged, payouts get delayed, and sometimes entire merchant accounts get suspended without much warning.

Businesses that accept international payments from customers around the world often face the same challenges as companies trying to accept global payments from overseas markets.Cross-Border Risk Flags

What we see in most cases is that businesses focus heavily on growth but underestimate how sensitive global payment networks actually are. The assumption that payment acceptance is purely a technical setup often leads to compliance gaps, inconsistent transaction patterns, and eventually account blocks. Even legitimate businesses face restrictions simply because their payment flow looks risky to banks or processors.

At FirmEU, we’ve observed that payment blocking is rarely a single-event issue. It is usually the result of small operational signals building up over time. Once flagged, recovery becomes significantly harder than prevention. That’s why understanding how global payments actually work is the first step toward building a stable, long-term payment infrastructure.

Prevent Payment Disruptions Early

Global payment systems do not fail suddenly. They fail gradually through small signals that go unnoticed. If your business is expanding internationally, now is the time to evaluate your payment setup before risk signals escalate into account restrictions.

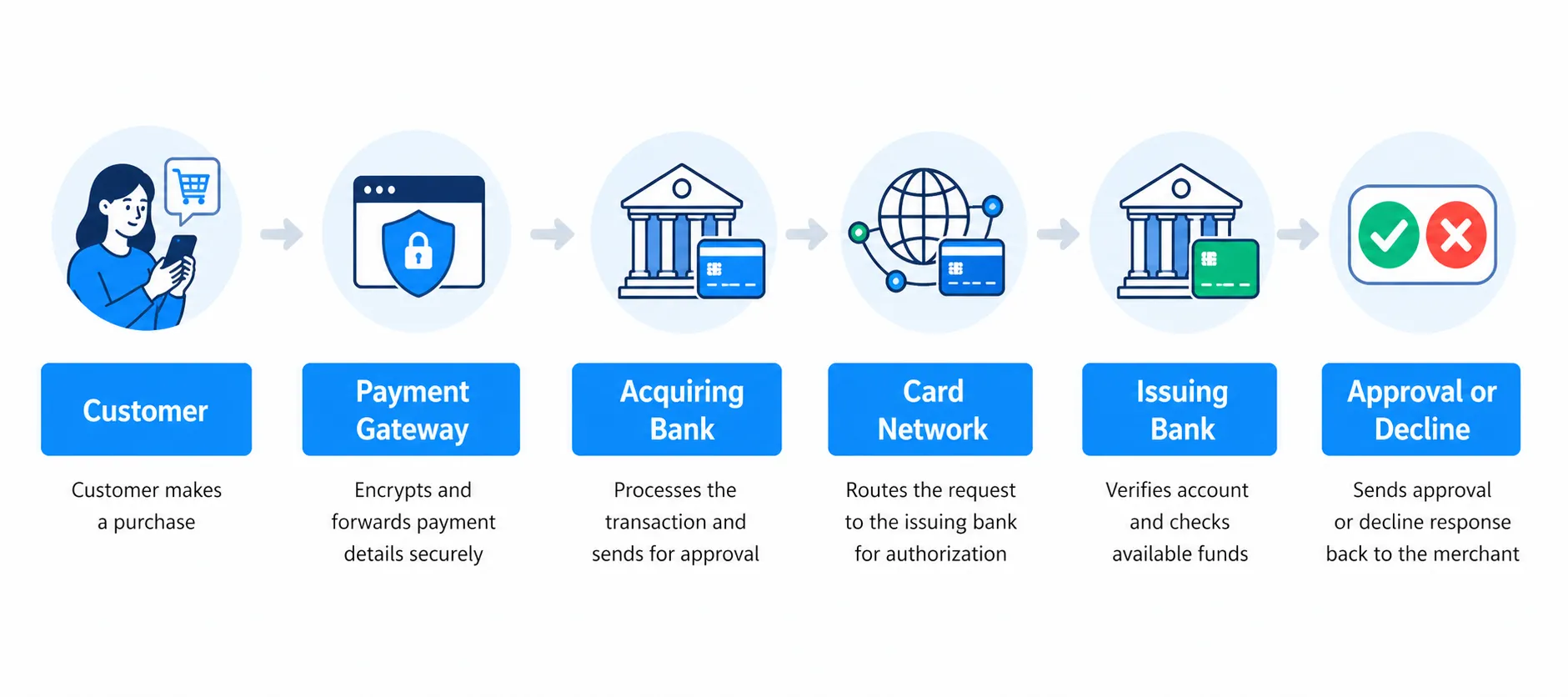

Understanding Global Payments Flow

Global payment acceptance is not a single system. It is a chain of multiple entities working together, including acquiring banks, issuing banks, card networks, and payment gateways. When a customer makes a payment, the transaction is checked at multiple levels before approval. Each checkpoint evaluates risk, geography, transaction behavior, and business category.

In simple terms, your payment does not just depend on your customer having funds. It depends on how trustworthy your business looks to the entire financial network.

Internal reference: Learn more about compliance structure in our guide on global payment compliance fundamentals.

At a basic level, the flow works like this:

Any weak signal in this chain can trigger friction or blocking.

Why Payment Blocks Actually Happen

Payment blocks are not random. They are usually triggered by a combination of risk indicators that build up over time.

Businesses often misunderstand this and assume it is a technical failure. In reality, it is a risk-based decision made by financial institutions.

The Real Cost of Payment Blockage

When a payment system gets blocked, the impact goes far beyond failed transactions. It affects revenue flow, customer trust, and even long-term partnerships with banks.

Here is how the impact typically spreads across a business:

What makes this more serious is the compounding effect. A single block can trigger additional scrutiny across all payment channels you use.

From what we’ve seen, businesses often recover revenue but lose access to a stable payment infrastructure for months.

Common Reasons Payments Get Blocked

Understanding the root causes is essential before you can fix or prevent blocks. Most issues fall into predictable patterns.

1. High-Risk Transaction Patterns

When a business suddenly receives high-value transactions, international spikes, or irregular payment volumes, it can trigger fraud detection systems. Even legitimate growth can appear suspicious if it lacks consistency.

2. Weak Business Classification

Every merchant is assigned a MCC (Merchant Category Code). If your business activity does not align with your declared category, banks flag it as mismatch risk. This is one of the most common hidden causes of blocking.

3. Poor Chargeback Management

High chargeback ratios signal dissatisfaction or fraud risk. Even a small percentage increase can push a business above acceptable thresholds, leading to account suspension.See how disputes affect stability in chargeback prevention strategies.

4. Cross-Border Risk Flags

International transactions carry a higher risk due to fraud probability differences across regions. Sudden global expansion without proper routing can trigger automatic holds. This is particularly common among companies trying to accept international payments at scale without first adapting their payment infrastructure. Optimize Payment Routing

5. Inconsistent Payment Behavior

Irregular transaction timing, unusual refund rates, or sudden spikes in failed payments often get flagged by monitoring systems.

6. Weak Compliance Setup

Missing KYC documentation, unclear refund policies, or incomplete business verification can result in immediate restrictions. Explore how regulatory compliance in sensitive industries like CBD directly influences payment approvals, risk scoring, and long-term processor stability.

7. Processor Sensitivity Differences

Not all payment providers have the same risk tolerance. Some are highly conservative and will block early instead of managing risk later.

Early Warning Signs of Blocking

Payment blocks rarely happen instantly. There are usually early indicators that most businesses ignore.

Increase in Soft Declines: Soft declines mean the transaction was not fully rejected but flagged for review. This is often the first sign of risk scoring changes.

Delayed Settlements: If payouts start taking longer than usual, it usually indicates additional internal verification is happening.

Sudden Verification Requests: Frequent requests for documents or transaction proof indicate rising risk assessment.

Drop in Approval Rates: A gradual decline in successful payments suggests issuer-side hesitation.

Increased Fraud Checks: Extra authentication steps such as OTP or 3D Secure appearing more often signal tightening controls.

Partial Holds on Funds: Funds being temporarily withheld is a strong indicator that the account is under review.These signals are early warnings that should not be ignored. They usually precede more serious restrictions. Discover why cross-border payments fail or get delayed without obvious errors, especially when routing and issuing bank signals start weakening.

Proven Strategies to Prevent Blocks

Preventing payment blocks is less about reacting and more about designing a stable system from the start.

1. Maintain Consistent Transaction Flow

Banks prefer predictable patterns. Avoid sudden spikes in volume without gradual scaling. Consistency builds trust across the system.

2. Strengthen Business Verification

Ensure all documentation, licensing, and compliance data are complete and up to date. This reduces unnecessary review triggers.

3. Optimize Payment Routing

Using multiple processors or smart routing can reduce dependency on a single risk system. It also improves approval rates across regions. Effective cross border payment processing depends heavily on how transactions are routed and monitored across different markets.

4. Control Chargeback Ratios

Implement proactive refund handling and clear customer communication to reduce disputes before they escalate.

5. Align MCC Classification Correctly

Ensure your business category accurately reflects your actual operations. Misclassification is a silent blocker.

6. Use Region-Based Risk Segmentation

Separate high-risk regions from low-risk regions to avoid global contamination of risk scores.

7. Improve Checkout Transparency

Clear pricing, refund policies, and billing descriptors reduce confusion-driven disputes.

Internal link: Explore system setup approaches in payment architecture for global merchants.

8. Monitor Payment Analytics Weekly

Track approval rates, decline reasons, and fraud signals consistently. Early detection prevents escalation. Discover how high-risk businesses structure their payment systems to avoid sudden freezes, manage processor sensitivity, and maintain global transaction flow.

Deep Operational Payment Flow

A stable global payment system is not just about gateways. It is about how your entire payment ecosystem is structured.

Most high-performing businesses use layered payment infrastructure. This approach supports global payment processing for businesses by reducing operational risk while maintaining consistent approval rates across multiple regions.. This includes:

- Multiple acquiring banks across regions

- Smart routing based on transaction type

- Fraud detection at pre-authorization stage

- Automated retry logic for failed transactions

- Currency-specific optimization

The goal is not just acceptance, but stability under scale. Businesses that want to accept payments online global markets often need stronger compliance controls, localized routing, and diversified acquiring relationships.

Operationally, businesses should also separate:

- Subscription payments

- One-time transactions

- High-value B2B payments

Each of these behaves differently in risk scoring systems.

A well-designed flow reduces false positives and improves long-term approval consistency. To understand how setup choices affect performance, it’s important to look at multi-currency and local accounts and how each impacts global expansion speed, fees, and overall payment acceptance stability.

Payment Misconceptions and Reality

Many businesses misunderstand how payment acceptance actually works.

“Any payment gateway will work globally”

Not true. Each gateway has different risk appetite, regional strengths, and industry restrictions.

“More gateways means better approval”

Not always. Poorly managed multiple gateways can create inconsistent data signals.

“Once approved, payments are safe”

Approval is dynamic. Your risk score changes continuously based on behavior.

“Only fraud causes blocks”

In reality, compliance gaps and behavioral anomalies are more common causes than fraud itself.

Understanding these differences helps businesses design more resilient payment systems.

Role of Payment Infrastructure Strategy

Your payment setup is not just a technical choice. It directly impacts business stability.

A strong infrastructure ensures:

- Reduced false declines

- Better global acceptance rates

- Lower fraud exposure

- Predictable cash flow

- Faster scaling into new markets

Businesses that want to accept payments globally without disruption must view payment infrastructure as a core growth function rather than a simple processing tool.

At FirmEU, we often see that businesses do not fail because of lack of customers, but because their payment infrastructure cannot support their growth model.

Choosing the right combination of processors, compliance setup, and routing logic determines whether your global expansion is stable or blocked midway.

Still Facing Payment Blocks While Expanding Globally?

WIf your current setup can’t handle cross-border complexity, it will eventually slow down your revenue and create instability. The right infrastructure doesn’t just process payments—it protects your growth at scale.

FAQs

Why do global payments get blocked suddenly?

Most blocks are triggered by accumulated risk signals like inconsistent transactions, compliance gaps, or high chargeback ratios rather than a single issue.

Do all payment gateways support global payments?

No, each gateway has different regional coverage and risk tolerance.

Do international payments increase blocking risk?

Yes. Cross-border payments are more closely monitored due to higher fraud exposure and regional risk differences.

How can I reduce payment declines?

You can improve approval rates by ensuring compliance accuracy, optimizing routing, and maintaining consistent transaction patterns.

What is the most common reason for payment failures?

The most common cause is a mismatch between business activity and the declared merchant category, followed by chargeback issues.

No. FirmEU is not a bank or financial institution. We operate as an independent matchmaking platform, connecting businesses with verified financial partners. All onboarding, KYC, and approval decisions are handled directly by the financial institution.

Still Have Questions?

Our sales team would be more than happy to assist with any futher inquiries

Contact Us

International Payment Solutions

Find the Right Banking and Payment Processing Partner for Your Business

Tell us about your company, and we’ll match you with the most suitable global banking or payment providers from our verified network.

Get Matched