How to Set Up Payment Processing for a High-Risk Business

Garry

April 24, 2026

1

minutes

Most merchants assume that setting up payment processing is a straightforward step. You register your business, apply with a payment provider, and start accepting transactions. But for high-risk businesses, this process is anything but simple.

High-risk businesses like gaming, adult services, supplements, crypto, and subscription-based models often face stricter scrutiny from banks and payment processors. What we see in most cases is that businesses underestimate how complex approval and ongoing compliance can be.

At FirmEU, we’ve seen that payment processing for high-risk businesses is not just about getting approved. It’s about building a system that can sustain approvals, reduce disruptions, and support growth across regions. Without the right setup, businesses face frequent account freezes, high fees, and sudden shutdowns. And once that happens, recovery becomes significantly harder.

If you’re operating in a high-risk category, the goal is not just to process payments. But it’s to build a payment infrastructure that works reliably under scrutiny.

Is your international payment setup becoming harder to manage?

When systems become fragmented, costs rise and control drops. A well-structured approach can simplify cross-border flows and make scaling smoother.

Understanding High-Risk Payment Processing

High-risk payment processing refers to payment systems designed for businesses that are more likely to face chargebacks, regulatory scrutiny, or financial instability. These businesses are categorized as high-risk due to:

- Industry Type

- Transaction Patterns

- Geographic Exposure

- Chargeback history

Unlike standard businesses, high-risk merchants often cannot rely on a single payment provider. They need specialized merchant accounts, a reliable high risk payment gateway, alternative payment methods, and backup systems.

To understand how different gateway models operate across regions, you can review Types of Cross-Border Payment Gateways. This setup is not optional. It is foundational.

The Real Cost of Poor Setup

Many businesses only realize the importance of proper setup after facing issues. Poor payment infrastructure does not fail immediately. It fails gradually, and then all at once. What makes this more challenging is that early-stage problems often go unnoticed. A few failed transactions, slightly higher decline rates, or delayed settlements may seem manageable at first. But from what we’ve seen, these small inefficiencies compound quickly. Over time, they start affecting customer trust, cash flow predictability, and overall business stability. This is where most businesses underestimate the real impact. Here’s how it impacts operations:

In most cases, these systems are interconnected. One weak point in the payment flow can trigger a chain reaction across approvals, settlements, and customer experience. For example, higher chargebacks can lead to stricter controls from processors, which then increase decline rates. This directly impacts conversions and revenue. Similarly, limited payment options reduce global reach, which restricts growth even if demand exists. This is why payment setup should not be treated as a one-time task. It is an ongoing system that needs to be built with resilience, flexibility, and long-term scalability in mind.

Where High-Risk Payment Setups Go Wrong

From what we’ve seen, failures are rarely random. They usually come down to predictable gaps in setup.

- Choosing the Wrong Payment Provider

Many businesses apply to standard processors that are not built for high-risk categories. This leads to rejections or short-term approvals followed by shutdowns.

- Lack of Business Transparency

Incomplete or inconsistent information about business models, revenue streams, or ownership structures raises red flags during underwriting.

- Weak Chargeback Controls

High-risk businesses naturally face more disputes. Without systems to monitor and reduce chargebacks, accounts quickly become unsustainable. For a deeper breakdown of reducing disputes, you can explore the ways to prevent chargebacks as a merchant.

- No Multi-Provider Strategy

Relying on a single processor creates a single point of failure. When that account goes down, revenue stops completely.

- Poor Checkout Experience

Limited payment options, slow processing, or frequent declines lead to customer drop-offs and reduced trust.

A strong checkout often depends on offering region-specific payment methods, which is covered in this guide.

- Ignoring Compliance Requirements

Regulatory frameworks vary by region. Missing compliance requirements can result in penalties or account suspensions.

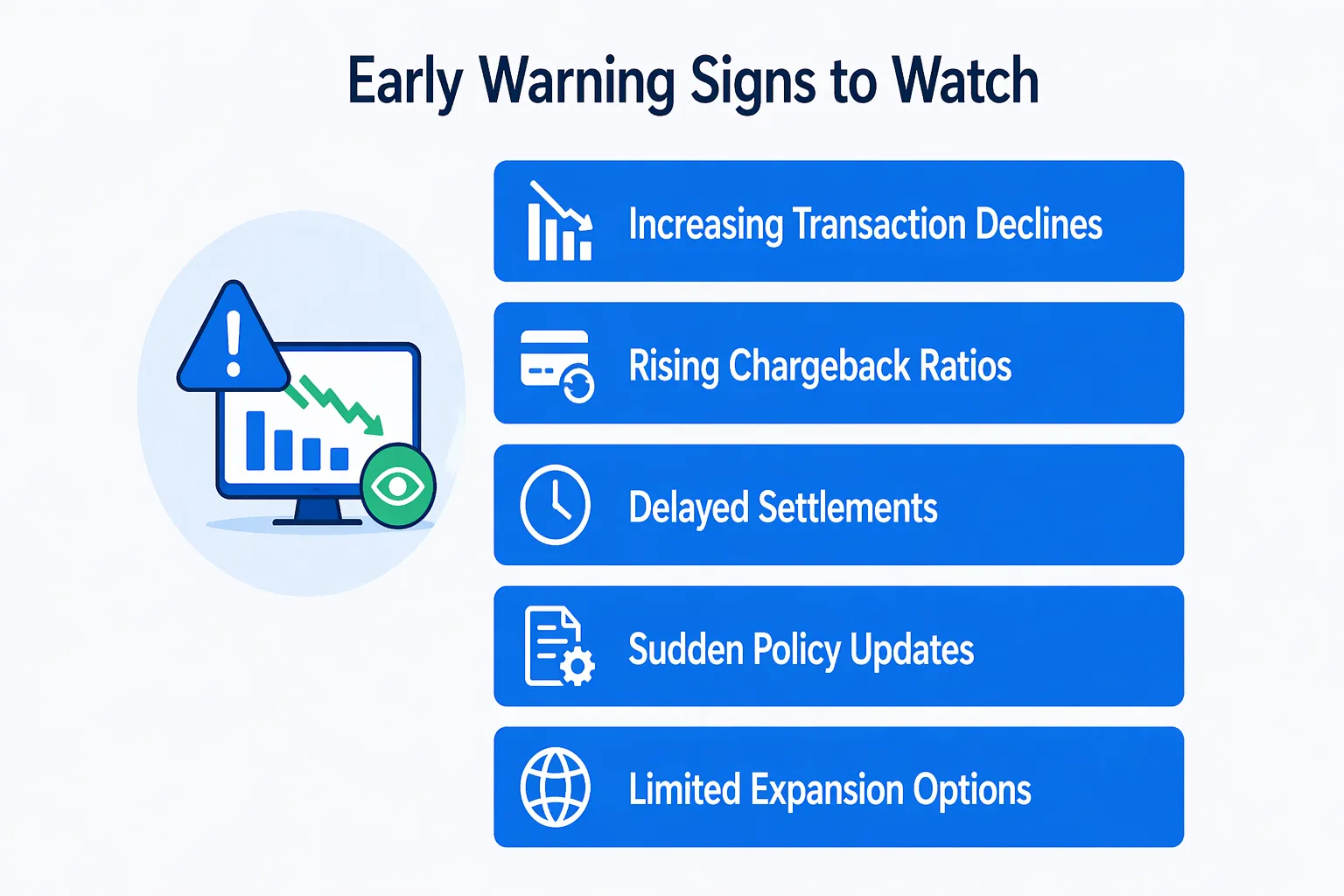

Early Warning Signs to Watch

Payment system issues rarely appear overnight. There are early indicators that signal deeper problems.

Increasing Transaction Declines

If approval rates start dropping, it often means that the processor is tightening risk controls.

Rising Chargeback Ratios

Even a small increase can push your account into a higher risk category.

Delayed Settlements

When payouts take longer than usual, it may indicate internal reviews or concerns from the provider.

Sudden Policy Updates

Frequent changes in terms and conditions often signal that the provider is reassessing your risk profile.

Limited Expansion Options

If your provider restricts certain geographies or currencies, scaling becomes difficult. In many cases, these limitations are tied to broader cross-border payment failures.

Recognizing these signs early allows you to take corrective action before disruptions impact revenue.

Proven Strategies for High-Risk Payment Setup

Setting up payment processing correctly requires a structured approach. It is not about finding a single solution, but building a resilient system.

- Collaborate with High-Risk Specialized Providers

Choose providers that specialize in high-risk industries. They understand the nature of your business and are more likely to offer stable, long-term solutions.

- Build a Multi-Account Setup

Use multiple merchant accounts across different providers. This reduces dependency and ensures continuity if one account faces issues. A detailed implementation approach can be found here.

- Implement Strong Chargeback Management

Use tools and processes to monitor disputes, respond quickly, and reduce future chargebacks. This directly impacts approval stability.

- Optimize Checkout Flow

Offer multiple payment methods, including cards, wallets, and local options. A flexible checkout improves conversion and reduces friction.

- Maintain Clear Documentation

Ensure all business details, financial records, and compliance documents are consistent and up to date. Transparency improves trust with providers.

- Use Payment Routing Logic

Smart routing directs transactions through the most suitable processor based on geography, currency, or risk level, helping businesses maximize the performance of their high risk payment gateway infrastructure.

- Plan for Geographic Expansion

Set up payment systems that support multi-currency and cross-border transactions from the start. Scaling becomes easier when infrastructure is already in place.

Payment Flow and Backend Optimization

A strong payment setup goes beyond approval. It includes how transactions move through your system.

Key areas to focus on:

- Transaction routing

- Fallback systems

- Fraud Filters

- Settlement tracking

Businesses expanding internationally should also consider multi-currency payment processing platforms to maintain consistency across regions. This backend layer is what keeps operations stable even under pressure.

It also plays a critical role in delivering secure payment processing for high-risk industries, where fraud prevention, compliance monitoring, and transaction reliability must work together to support long-term growth.

High-Risk vs Standard Payment Setup

Many businesses assume high-risk processing is just a more expensive version of standard processing. That’s not accurate. Here’s what actually differentiates the two:

Standard Setup:

- Single Provider

- Lower Fees

- Minimal compliance checks

High-risk setup:

- Multiple providers

- Higher fees but higher tolerance

- Continuous monitoring and compliance

The difference is not just cost. It is complexity and control.

Role of the Right Payment Partner

Choosing the right partner for high risk payment processing services plays a critical role in how your payment system performs over time.

In most cases, businesses struggle because they try to manage everything independently without understanding how processors evaluate risk. A structured partner helps with:

- Matching your business with suitable providers

- Preparing documentation for approvals

- Designing multi-account setups

- Ensuring compliance across regions

At this stage, the goal is not just approval. It is long-term stability.

To Sum Up

Setting up payment processing for a high-risk business is not just about getting approved. It is about building a system that works reliably over time. With the right providers, multiple accounts, and strong compliance, you can avoid disruptions and keep payments running smoothly. At FirmEU, the focus is on creating stable payment setups that support long-term, not short-term approvals.

Struggling to get stable payment processing for your high-risk business?

The right setup can make the difference between constant disruptions and predictable growth.

FAQs

What makes a business high-risk for payment processors?

Industries with high chargebacks, regulatory complexity, or subscription models are typically classified as high-risk.

Can high-risk businesses use standard payment gateways?

In most cases, standard gateways either reject applications or provide short-term approvals that are not sustainable.

Why are chargebacks such a big issue?

High chargeback ratios signal risk to processors and can lead to penalties, higher fees, or account termination.

Is it necessary to have multiple payment providers?

Yes, relying on one provider increases risk. Multiple accounts ensure continuity and reduce downtime.

How long does approval take for high-risk accounts?

It varies, but approvals typically take longer due to stricter verification and underwriting processes.

No. FirmEU is not a bank or financial institution. We operate as an independent matchmaking platform, connecting businesses with verified financial partners. All onboarding, KYC, and approval decisions are handled directly by the financial institution.

Still Have Questions?

Our sales team would be more than happy to assist with any futher inquiries

Contact Us

International Payment Solutions

Find the Right Banking and Payment Processing Partner for Your Business

Tell us about your company, and we’ll match you with the most suitable global banking or payment providers from our verified network.

Get Matched