How to Set Up a SEPA Direct Debit for Your Business: The Complete, Step-by-Step Guide

Roan Dollmann

September 19, 2025

1

minutes

Setting up a SEPA Direct Debit is an essential step for any business that wants to collect payments efficiently across Europe.

Whether you are an e-commerce brand, a SaaS provider, or a high-risk business expanding into the EU, understanding how to set up a SEPA Direct Debit correctly can help you simplify collections, improve cash flow, and reduce payment failures.

This guide covers everything - from activating SEPA for your business to integrating it with your payment systems.

By the end, you’ll know exactly how to enable SEPA payments while staying fully compliant with Eurozone regulations.

What is SEPA Direct Debit?

SEPA Direct Debit is a simple and secure way to pay bills or subscriptions in euros across many European countries.

When you use SEPA Direct Debit, you give permission - called a mandate - to a company to take money directly from your bank account to pay for something, like a phone bill or gym membership.

This can happen once or on a regular schedule, without you having to do anything every time.

There are two types:

- SEPA Core Direct Debit: Designed mainly for consumers, it offers protections such as an 8-week refund window for authorized debits and up to 13 months for unauthorized transactions.

- SEPA B2B Direct Debit: Used for business-to-business transactions. It requires stricter mandate validation and offers limited refund rights, relying on trust between companies.

This system helps businesses by making payments easier and faster across different European countries, and it keeps payments safe through clear rules and ways to check transactions.

In short, it's a handy way to pay in euros that works across borders without needing cash or cards.

How to Set Up SEPA Direct Debit: A Complete Step-by-Step Guide for Businesses

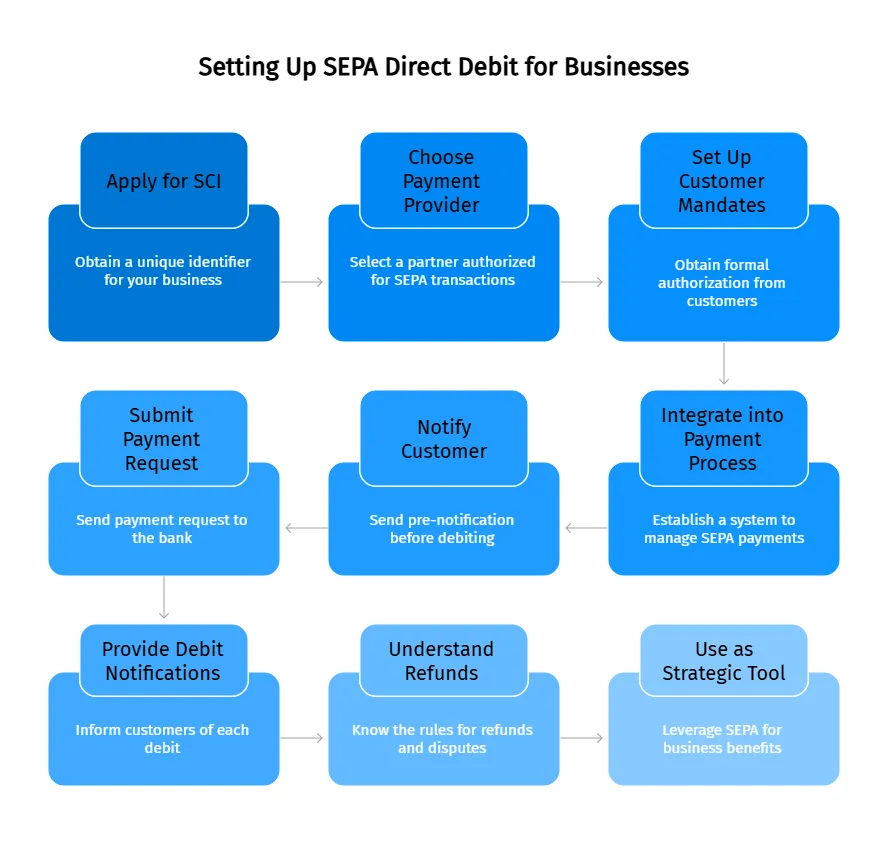

Step 1: Apply for a SEPA Creditor Identifier (SCI)

Your first step is to obtain a SEPA Creditor Identifier (SCI).

This is a unique number that identifies your business when you collect payments by SEPA Direct Debit.

You will use this number in every SEPA mandate and payment file.

Where to get it:

- In most European countries, your business bank can issue this for you.

- In some countries, you’ll need to apply through your national central bank or designated authority.

Step 2: Choose a SEPA-Enabled Payment Provider

To process SEPA Direct Debit transactions, you need a partner that is authorized to handle them.

This can be:

- A traditional business bank

- A fintech payment platform

- A specialized provider that works with high-risk or international industries (e.g. crypto, gaming, forex, adult)

How to decide:

Your choice should be based on your business type, industry risk level, customer base, and location.

Step 3: Set Up Customer Mandates

A SEPA mandate is a formal authorization from your customer allowing your business to debit their bank account.

Without a valid mandate, you cannot collect payments.

There are two types:

- Paper mandate: Signed physically by the customer

- Electronic mandate (eMandate): Completed and approved online

Each mandate must include the following elements:

- Your Creditor Identifier (SCI)

- A Unique Mandate Reference (UMR) — this must be unique for each customer and unique under your SCI. It can contain up to 35 characters.

- The customer’s name and IBAN

- The date of authorization

- A signature or electronic approval with timestamp

You must keep a record of every mandate, securely and in a way that allows you to retrieve it if requested by a bank or during a dispute.

Mandates are not typically sent to the bank unless specifically required.

Step 4: Integrate SEPA Direct Debit Into Your Payment Process

Once mandates are collected, your business needs a system in place to manage SEPA payments.

This may involve:

- Collecting mandates via a form on your website or onboarding process

- Connecting your system to your payment provider (e.g. through an API, if available)

- Scheduling payments and managing payment notifications automatically

Step 5: Notify the Customer Before Charging

You must send a pre-notification to the customer at least 14 days before you collect the first payment, unless a shorter period has been agreed.

The pre-notification must include:

- The amount to be debited

- The date of the debit

- The mandate reference (UMR)

- Your Creditor Identifier (SCI)

- Optionally, a reference to the invoice(s) being paid

This can be sent via email, letter, or included in the invoice, as long as it's documented.

The purpose is to give the customer time to raise any questions or objections before the funds are collected.

Step 6: Submit the Payment Request to Your Bank

After the mandate is in place and the customer has been notified, you (or your payment provider) will submit the payment request to your bank.

This is done using a standardized SEPA Direct Debit file, typically in XML format (PAIN.008).

Deadlines for submission:

- Core SEPA Direct Debit (used for consumers): Submit at least 1 business day before the payment date

- B2B SEPA Direct Debit (used between businesses): Some banks allow same-day submissions, depending on the provider

Your payment partner will usually handle the file format and submission details for you.

Step 7: Provide Ongoing Debit Notifications

While the initial pre-notification is required, it is also considered best practice to inform your customers each time a debit is made.

This improves transparency and reduces the chance of disputes.

Each notification should include:

- The amount charged

- The date of debit

- The mandate reference (UMR)

- Reference to the invoice or service being paid

This step is especially valuable for businesses using SEPA for subscriptions or recurring billing.

Step 8: Understand Refunds and Customer Rights

SEPA Direct Debit includes consumer protection rules, especially for Core (B2C) transactions.

Refund periods:

- Consumers (Core SDD):

- Customers can request a refund for any reason within 8 weeks of the debit

- If the debit was unauthorized, they can dispute it for up to 13 months

- Customers can request a refund for any reason within 8 weeks of the debit

- Businesses (B2B SDD):

- Once processed, payments are non-refundable, unless both parties agree

What happens during a refund:

If a customer disputes a payment and the bank approves the refund, the full amount is reversed.

Your business account is debited again, and the customer is credited back, even months later.

This is why it’s important to use SEPA Direct Debit with reliable, trusted customers, especially for large transactions.

Step 9: Consider SEPA Direct Debit as a Strategic Tool

Beyond just a payment method, SEPA Direct Debit can help your business:

- Improve cash flow stability

- Reduce manual invoicing and delays

- Decrease payment failures compared to card payments

- Strengthen accounts receivable management

However, not every customer may be comfortable with direct debits. Some may prefer manual payments or card payments.

For this reason, it’s best to offer SEPA Direct Debit to customers you have an ongoing relationship with, where trust is already established.

What Is a SEPA Direct Debit Mandate Template and Why Does Your Business Need One?

A SEPA Direct Debit mandate template is a standardized document used to obtain formal authorization from a customer (the debtor) to allow a business (the creditor) to collect payments directly from their bank account.

This template ensures that the agreement between both parties is clear, documented, and fully compliant with SEPA regulations.

Using a mandate template helps businesses establish a structured and transparent payment process.

It outlines when payments will be collected, under what conditions, and for which services or invoices.

This clarity reduces the risk of disputes, delays, or failed payments.

Key Benefits of Using a SEPA Mandate Template:

- Regulatory Compliance:

The template ensures that your mandate includes all required legal elements, such as the creditor identifier (SCI), unique mandate reference (UMR), debtor’s IBAN, and authorization date.

This helps your business stay compliant with SEPA standards. - Payment Predictability:

Customers know in advance when amounts will be charged and for what purpose.

This improves their ability to manage finances and reduces the likelihood of chargebacks or objections. - Improved Cash Flow Planning:

Businesses benefit from predictable payment dates and better control over incoming funds, which supports more efficient financial planning and operations. - Strengthened Trust Between Parties:

A clearly worded, standardized mandate fosters transparency and trust. Both the creditor and debtor understand their roles and obligations, creating a smoother long-term business relationship. - Support for Recurring Payments:

Once authorized, a SEPA mandate can be used for future transactions without requiring new approval every time, making it ideal for subscription models or ongoing services.

In summary, a SEPA Direct Debit mandate template is not just an administrative form, it’s a foundational tool that simplifies collections, supports compliance, and builds trust.

Businesses that collect payments in euros across Europe should use a proper mandate template to ensure a professional, secure, and efficient payment process.

Can I Use SEPA Direct Debit in Any Country?

No. SEPA Direct Debit can only be used within SEPA zone countries, and the account used must be opened in the same region where the SEPA payment will take place.

For example, you cannot use a SEPA Direct Debit from a USD account in the US, nor can you initiate a SEPA debit from an account opened outside the SEPA area.

To use SEPA Direct Debit, your account must be denominated in EUR and located in a SEPA-compliant country.

What Currencies Are Supported for SEPA Direct Debit?

The SEPA Direct Debit system only supports payments in euros (EUR). Other currencies, like USD or GBP, are not accepted within SEPA Direct Debit transactions.

If you're working with customers in the UK, you can use GBP for UK Direct Debits, but that would fall under the UK’s domestic direct debit system, not SEPA.

Can I Set Up SEPA Direct Debit Payments Through My Business Bank Account?

Yes, but with some limitations.

Businesses cannot always initiate or configure SEPA Direct Debits directly through their online banking interface, especially with digital or fintech banks.

Instead, you must usually:

- Contact the payee or merchant (if you're the customer).

- Provide them with your EUR IBAN and BIC.

- Sign a mandate authorizing them to debit your account.

If you're a business collecting payments, you will need a SEPA-enabled payment provider or business bank that supports the initiation of outbound SEPA Direct Debits.

Are There Fees for Setting Up SEPA Direct Debit?

Most banks and payment providers do not charge a fee to set up SEPA Direct Debit mandates.

However, currency conversion fees may apply if you're dealing with customers or accounts outside the eurozone.

It's also important to review your provider’s pricing model for transaction processing, failed debits, or chargebacks.

Can I Transfer a SEPA Direct Debit to Another Account?

No, SEPA Direct Debits cannot be transferred between different bank accounts. If your business or customer changes their bank details, the existing mandate becomes invalid.

In that case:

- The customer must provide the new account details to the merchant.

- A new mandate must be created and authorized for the updated account.

This ensures that SEPA rules are followed and that both parties are protected under the correct agreement.

Can I Set Up SEPA Direct Debits for Outbound Payments?

Yes, as a customer (debtor), you can authorize a business to deduct funds from your account using SEPA Direct Debit. This is called an outbound SEPA Direct Debit from your perspective.

However, not all banks allow customers to initiate these setups directly from their account interface.

Some digital banks do not support inbound SEPA Direct Debits (i.e., collecting payments from others), but they do allow outbound payments.

Always check whether your bank supports the type of SEPA Direct Debit you need, inbound (to receive payments) or outbound (to pay others).

Final Tip: Choose the Right Banking and Payment Setup

Understanding the operational and technical limitations of SEPA Direct Debit is key to choosing the right banking partner or payment provider.

Whether you're collecting payments across Europe or authorizing recurring charges from your own account, make sure your provider:

- Supports both Core and B2B SEPA schemes

- Allows inbound and outbound debits where needed

- Provides clear mandate management and reporting tools

- Ensures compliance with SEPA regulations

Can I use SEPA Direct Debit if my customer’s bank is outside the Eurozone?

SEPA Direct Debit requires both the creditor’s and debtor’s bank accounts to be located within the SEPA zone, which currently includes 41 countries, most of which use the euro.

Non-euro countries in SEPA also participate, but the payment must be in euros and the debtor’s account must be SEPA-compliant.

If your customer’s bank is outside the SEPA area or does not support SEPA payments, you cannot use SEPA Direct Debit with them.

What is The Difference Between SEPA Direct Debit Core and B2B Schemes in Simple Terms?

The Core scheme is for collecting payments from consumers and offers strong consumer protections like refund rights up to 8 weeks (and 13 months for unauthorized payments).

The B2B scheme is for business-to-business transactions with stricter rules and almost no refund rights after payment, relying on upfront mandate verification. Choose Core for most customer payments unless you clearly deal only with businesses.

Use SEPA the Right Way — With the Right Partner

Setting up SEPA Direct Debit correctly is critical for businesses operating in Europe, especially for high-risk industries like crypto, forex, or gaming that face stricter banking requirements.

At FirmEU, we specialize in guiding businesses through SEPA compliance, from securing creditor identifiers to integrating payment solutions with high-risk-friendly banks.

Our experts provide tailored support for international merchants needing reliable EUR payment processing, whether you're launching in the EU or scaling cross-border operations.

FAQs

No. FirmEU is not a bank or financial institution. We operate as an independent matchmaking platform, connecting businesses with verified financial partners. All onboarding, KYC, and approval decisions are handled directly by the financial institution.

Still Have Questions?

Our sales team would be more than happy to assist with any futher inquiries

Contact Us

International Payment Solutions

Find the Right Banking and Payment Processing Partner for Your Business

Tell us about your company, and we’ll match you with the most suitable global banking or payment providers from our verified network.

Get Matched