How to Integrate Multiple Payment Processors on Your Website?

Garry

April 2, 2026

1

minutes

A business founder came to us and told us everything was working fine, but suddenly, transactions were facing an issue. Transactions were failing and there was no clear reason why it was happening, no warnings, just declined payments. But when we checked thoroughly, it was exactly what we expected the reason to be - relying on a single payment processor.

I remember one e-commerce client was selling globally. His ads were performing well, steady traffic, but the conversion rate of leads was dropping overnight. It wasn’t because of the product or its pricing, but because of the failure of payments and transactions in certain nations. And this can impact your business terribly, no matter how well you are doing, but relying on a single source for your revenue transactions can actually be scary. It becomes scary for businesses that are operating in

- Cross-border e-commerce

- Subscription-based platforms

- High-risk businesses like crypto, 18+, or CBD

In these sectors, payment stability is not guaranteed. A payment processor can decline specific countries or regions. There can be changes in policies overnight. Or accounts can be restricted for review. We’ve seen it multiple times, especially when businesses start working and ranking internationally. This is the reason why successful businesses don’t rely on just one provider for payments. They build a setup into which, if one payment fails → another takes over. If one declines → another approves. And if one region is blocked → routing shifts automatically within the system.

It is more like having a backup plan. Let’s say you are flying an airplane. And one engine stops working, if you were relying on one single engine you're cooked for sure. But if you have a backup engine already, then you can use that. Easy, right?

At FirmEU, when we speak with clients, we don’t start with “which processor do you want?” We start with:

“What happens if your current processor stops working tomorrow?”

Because that’s the real question and a more practical one. If you have already made sure of making a system that actually supports your growth instead of blocking it, you are more likely to win in the market.

Need a more reliable way to handle your payments?

FirmEU connects businesses with verified providers that support global transactions and complex payment needs..

When Do You Actually Need Multiple Payment Processors?

Let me be very honest here. Not every business needs multiple payment processors from day one. If you are just starting with something, selling locally, and everything is working fine, then one good provider can handle things. But when you start growing, patterns change, and this is where I usually tell clients, “ You aren’t supposed to add multiple processors when things break; you add them before they break.” And that’s what changes the game. Let’s talk in more detail:

Situation 1: You are selling in Multiple countries

This is the most obvious reason to get multiple processors. You go well when you start in one country, but with growth, strategies also need to grow. With the expansion of your business internationally, you can not expect one payment medium to behave the same in every country. Some methods can be smooth for Europe, but do not work at all in Asia. In the same way, some can work fine in Asian regions, but not in Europe. That’s why businesses that are handling cross-border payments are almost always moving towards multiple-processor setups.

Situation 2: You are Running a Subscription or Repetitive Model

Subscription-based platforms look easy, but the payments behind them are not simple. Issues we often see include recurring payment failures after the first cycle, cards getting declined randomly, and login retry not working properly. If you are dependent on one processor, recovery options get limited. But with multiple processors, you get multiple backup options. One payment failed; you can try another method. Recovery rates improve, and churn reduces silently.

Situation 3: You are in a High- Risk Industry

This includes industries like crypto, CBD, adult & dating, and financial services/MSBs, which are often categorized as high-risk business segments. These face very strict policies from processors. Some providers will not even onboard a few of these businesses, some will onboard but will limit transactions, and some may put accounts on restrictions or pause them for account review. We’ve seen such cases where businesses had to stop accepting payments overnight. The thing is, this is not a technical problem that can be fixed or just left as it is; this is, in fact, a business risk. This is exactly why multiple payment gateways for high-risk business models have become less of an option and more of a necessity, since one declined account can mean a complete revenue stop.

Situation 4: You are Growing Fast

Success is cool as long as you can handle it. Growth in business feels exciting until payments start behaving differently. We do everything to make money, but if money gets blocked, it feels like losing the game. I’ve come across so many clients like this - growing fast, ads trending, increasing traffic, increasing revenue, but suddenly, a huge impact on revenue. Nothing changes superfast in front, nothing is so obvious quickie, but the backend slowly starts getting impacted. As volume increases, there are more transactions and, therefore, more likely chances of fraud. Unusual spikes mean there can be flagged activities without getting noticed.

Cross-border mixing can lead to more declines. Also, high-volume transactions get noticed and monitored even more strictly. So ironically, growth can expose weakness in your payment setup. If everything depends on one processor, even a small change in its risk model can impact your entire revenue flow.

Different Ways to Integrate Multiple Payment Processors

When someone asks me this question, it is usually after they have already faced such an issue with transactions. Either approvals have dropped, or a processor has started creating troubles, or they’re expanding into new markets, and things are not as smooth as before. And then the question arises - “HOW DO WE ACTUALLY SET UP MULTIPLE PROCESSORS?”

The truth is, there is not just one single method to do it. The correct approach depends on how your business is structured, how fast you are growing, and how much control you want over your payment flow. The most basic way is direct integration. In this setup, your development team connects your website or app directly with multiple payment processors using their APIs. On paper, it looks very flexible because you are not dependent on any single provider. You can decide which processor handles which transaction, and you can build your own logic around it. But in reality, this comes with a responsibility. Every processor has its own API, its own rules and its own quirks. Maintaining multiple integrations takes time, and unless you have a strong technical team, things can quickly become messy. We have seen organisations start with this approach and then struggle to manage it once they start growing.

Then comes the second approach, which is more practical for most businesses. Instead of integrating multiple processors yourself, you use a payment gateway or aggregator that already connects to several providers. From your side, it feels like a single integration, but behind the scenes, there are multiple processors involved. This reduces development effort and speeds up the setup. However, in this case, you are also giving away some control; you do not always decide how transactions are routed, and in some cases, especially for high-risk or cross-border businesses, the available options can be limited. The third approach is what we are seeing more and more now, especially with your businesses that are growing internationally. This is where payment orchestration comes in. Instead of just connecting processors, you build a system that intelligently decides how payment should flow. Transactions are routed based on logic - the logic can be a location, card type, risk level or even past performance. If one processor fails to proceed, another automatically takes over. If approval drops in one region, routing can be adjusted without changing your entire setup.

It’s not just about having multiple processors. It’s about using them in a smart way. From what I have noticed in my experience with this, most businesses do not actually need the most complex setup from day one. What they need is clarity. The need to know which processors are actually suitable for their line of business, and how they can combine them without overcomplicating things. Also, they want to know how they can keep the system flexible to use as they scale. This is the core idea behind multiple payment gateway integration - building a setup that grows with the business rather than one that needs to be torn down and rebuilt every time the business scales.

At FirmEU, this is usually where we step in. Not by pushing a specific provider, but by helping businesses understand how different processors can work together based on their model, regions and transaction flow.

How Multi- Processor Systems Work Behind the Scenes

Whenever I explain this to clients, I don’t go into technical jargon. I ask in very simple, plain language - “What if your payment system is making decisions itself in real time without operating it?” Because this is exactly what is happening. When a customer clicks “Pay Now.” It’s not just one straight path anymore. In a multi-processor setup, your system evaluates the transaction and decides where it should go. Assume that if someone is from Germany, trying to make a payment on your website, rather than sending that transaction blindly to one single processor, the system selects the provider that performs better in Europe and routes it to that.

Now, assuming another customer from Southeast Asia, the same system can send that payment to a completely different processor that handles that region in a better way. Nothing actually changes at the front end. The customer will not see any difference. But in the backend, your system is quietly making every transaction better. This is what we can call smart routing in transactions. And it is not always based on geographical choices. The decisions include card type (VISA, Mastercard, Local Cards), transaction size (amount), risk score, and the use of secure transaction methods to ensure safer and more reliable payments.

With time, the system becomes faster as it’s automated to detect patterns. You know which processor works better in which situation. But here is another important layer - failover.

This is something that most businesses do not have, and they only realise that they need it when it’s too late. To understand it more easily-

Assume a transaction gets declined by Processor 1. In a normal setup, what would happen after this decline?

It’s normally THE END for a normal setup.

But, in the case of a multi-processor system, you can retry that same transaction through Processor 2, automatically. Sometimes, the same payment that failed once goes through successfully on the second attempt. It’s a small difference in setup, but a big difference in revenue. There is also something called load distribution, which becomes important when your volume increases. Rather than pushing all transactions through one processor, you spread them across multiple providers. This decreases the dependency and also helps you avoid the triggering risk checks that sometimes happen when too much volume flows through a single channel.

One thing I always like to tell businesses is - “ Payments are not just about accepting money. They are about approval optimization. And this is where multi-processor systems quietly improve performance without you even noticing. At FirmEU, we have seen businesses improve their approval rates simply by changing how transactions are routed. Neither by changing their product, nor by pricing changes, but by optimising the backend flow.

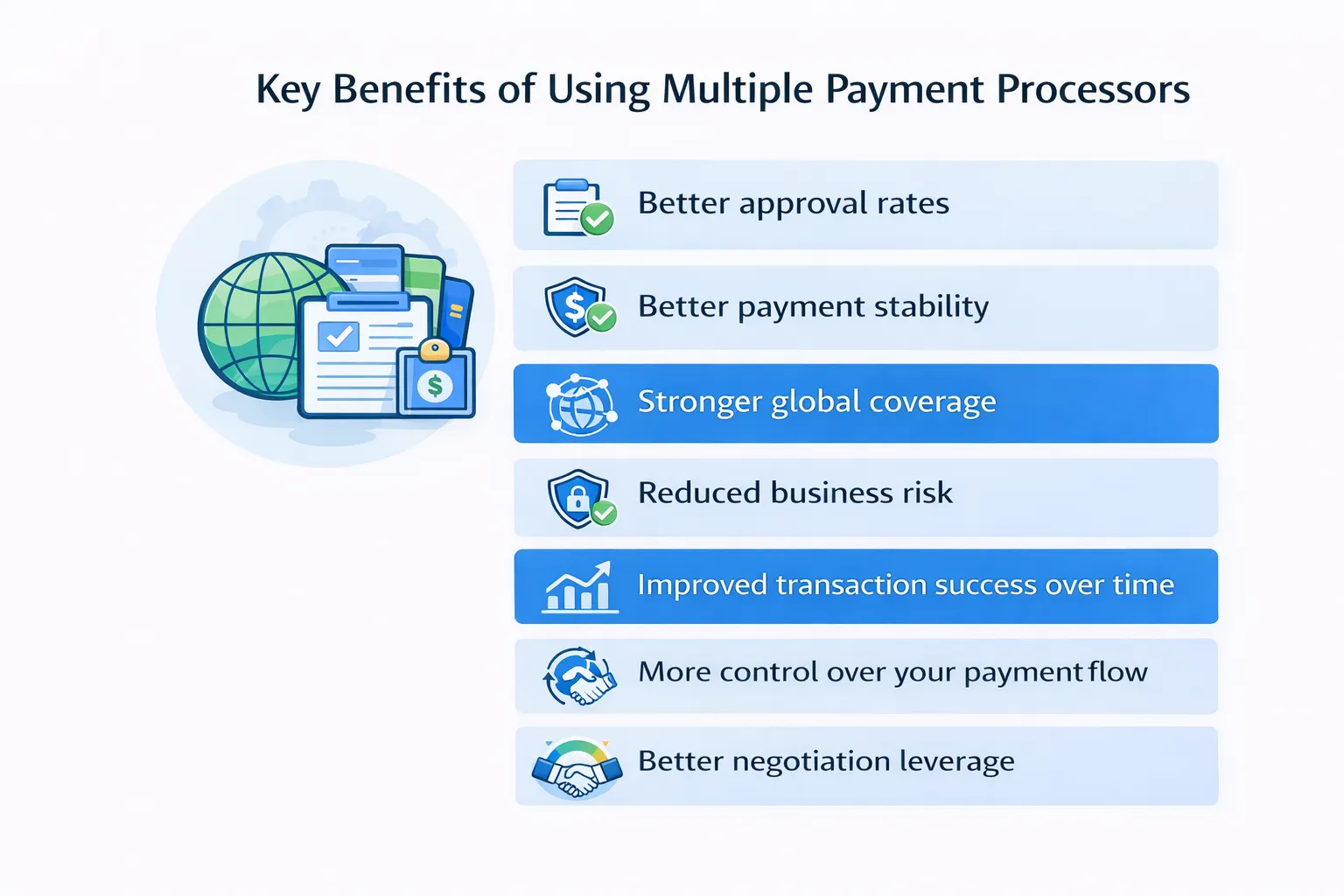

Key Benefits of Using Multiple Payment Processors

When businesses start considering multiple payment processors, they usually expect some technical improvements. But in reality, the biggest impact is on stability and revenue, which is actually a win. It is one of those backend decisions that does not look exciting, but once it is implemented, it quietly improves performance across your entire payment flow. I have seen businesses go from struggling in failed transactions to running smooth global operations just by restructuring how payments are handled. When you set it up the right way, here is what actually changes - the benefits of multiple payment gateways become visible across approval rates, stability, and long-term flexibility: Situation 3: You are in a High- Risk Industry

- Better approval rates: The same translation does not depend on a single processor anymore. There is always a backup; if one fails, the system will automatically route to a better option and complete the transaction.

- Better Payment Stability: Failures are reduced due to having backups, and payments keep getting successful through relevant options because of having more than one processor.

- Stronger Global Coverage: With multiple processors, you get to have different processors for each region, and this way, every time you make a payment, the system automatically chooses the better processor for the required region, rather than forcing one provider to handle everything.

- Reduced business risk: In case of high-risk industries, the system chooses the correct provider that aligns with requirements and avoids the risk of getting an account restricted or paused for review, preventing the transaction failures.

- Improved transaction success over time: Once you start routing payments smartly, with time, the system learns which processors work best in which scenario, so the process gets faster with time and improves gradually.

- More control over your payment flow: You are no longer dependent on the rules of one provider. You can choose how transactions should move based on your business requirements.

- Better negotiation leverage: When you have options, and you are no longer tied to only one provider, this means you can actually compare, shift volume, and negotiate better fees or terms.

Final Thoughts

If I have to mention one thing that I have learned while working with different businesses, I would say - Payments do not usually break suddenly. They slowly start showing signs, cracks, and by the time you notice, it is already affecting your revenue. Most businesses focus heavily on marketing their products and growth, but they forget the main thing. That is transaction flow. The real thing is, payment flow needs to evolve as the business grows. Setting up multiple payment processors is not about adding complexity; it is about building flexibility within your system so that your business does not stay dependent on one single provider. Different countries, different regulations, different payment behaviours - how will this be acceptable for one provider to fit in all?

Here at FirmEU, we do not just connect you with one provider and move on. We work with businesses to understand their model, regions, requirements, and transaction flow, and then help them build an end-to-end payment structure that actually works in the real world -especially across Europe. In some scenarios, it is about adding a second processor; in some, it is about restructuring the entire flow. Some citations require fixing and correcting what is already there.

If you are unsure whether your current setup can handle your growth, it is worth having that conversation early rather than waiting for a problem to force your change the whole setup after the loss.

Looking to scale without payment disruptions?

FirmEU helps you connect with trusted processors and banking partners that support growing businesses.

FAQs

What are multiple payment gateways?

Multiple payment gateways allow businesses to process transactions through more than one provider to reduce failures and improve approvals.

Why should I use multiple payment gateways?

They improve payment success rates, reduce downtime, and help manage global transactions more efficiently.

How do you integrate multiple payment gateways?

You connect your website to more than one provider through direct API integration, an aggregator, or an orchestration layer that routes transactions based on logic like location, card type, and success rates to the best-performing provider.

Is using multiple gateways expensive?

It can increase setup costs but often improves revenue enough to outweigh the expense.

What is payment orchestration?

It’s a system that automatically routes payments to the most suitable processor in real time.

No. FirmEU is not a bank or financial institution. We operate as an independent matchmaking platform, connecting businesses with verified financial partners. All onboarding, KYC, and approval decisions are handled directly by the financial institution.

Still Have Questions?

Our sales team would be more than happy to assist with any futher inquiries

Contact Us

International Payment Solutions

Find the Right Banking and Payment Processing Partner for Your Business

Tell us about your company, and we’ll match you with the most suitable global banking or payment providers from our verified network.

Get Matched