CBD Payment Processing Compliance: What CBD Businesses Need to Know

Garry

March 9, 2026

1

minutes

.webp)

The CBD industry is expanding quickly, with many companies selling oils, cosmetics, and wellness products across multiple markets. However, one major challenge most CBD businesses face is payment processing for CBD.

Even when CBD products are legal, many banks and payment processors classify CBD merchants as high-risk CBD businesses. This often leads to declined merchant applications, strict compliance checks, settlement delays, or sudden account closures.

At FirmEU, we regularly speak with CBD founders who struggle to secure stable payment infrastructure. Many processors hesitate to support CBD & cannabis payment processing because regulations differ across regions and compliance requirements are complex.

This is why CBD businesses must understand CBD payment processing compliance early. With the right structure and the right financial partners, companies can build a stable and compliant payment system for global operations.

Need reliable CBD payment processing support?

FirmEU connects CBD companies with verified payment processors and banking partners that already support regulated industries.

Why Many Payment Processors Reject CBD Businesses

Even though the CBD market has become more accepted in recent years, many payment processors still hesitate to work with CBD companies. The main reason is risk management. Financial institutions carefully evaluate industries that may carry regulatory uncertainty, reputational concerns, or complex compliance requirements.

Main reasons for Rejections

Regulatory Inconsistency

One of the biggest concerns is regulatory inconsistency. CBD regulations vary significantly between countries and sometimes even between states or regions within the same country. Payment providers must ensure that transactions comply with local laws, THC limits, labeling standards, and product classifications. If a processor cannot clearly determine whether a business meets these requirements, they often choose to reject the application rather than take the risk.

Compliance Monitoring Requirements

Another factor is compliance monitoring. CBD merchant account applicants typically require more documentation than standard e-commerce businesses. Processors may request product certificates, laboratory reports, licensing documents, and detailed descriptions of the business model. If these documents are incomplete or unclear, the onboarding process may stop immediately.Key Compliance Requirements for CBD Payment Processing

Transaction Pattern Risks

Transaction patterns also influence processor decisions. CBD businesses frequently operate online, sell across borders, and rely on digital marketing channels. These factors can trigger automated risk systems that monitor transaction velocity, refund ratios, and chargeback levels. When systems flag these patterns, applications may be declined or accounts may face ongoing reviews.

Because of these barriers, many CBD companies spend months contacting different processors without success. Instead of approaching providers individually, businesses often benefit from working with platforms that already maintain relationships with processors familiar with CBD transactions. Through networks of verified banking and payment partners, companies can connect with providers that understand the compliance requirements associated with CBD-related payment flows.

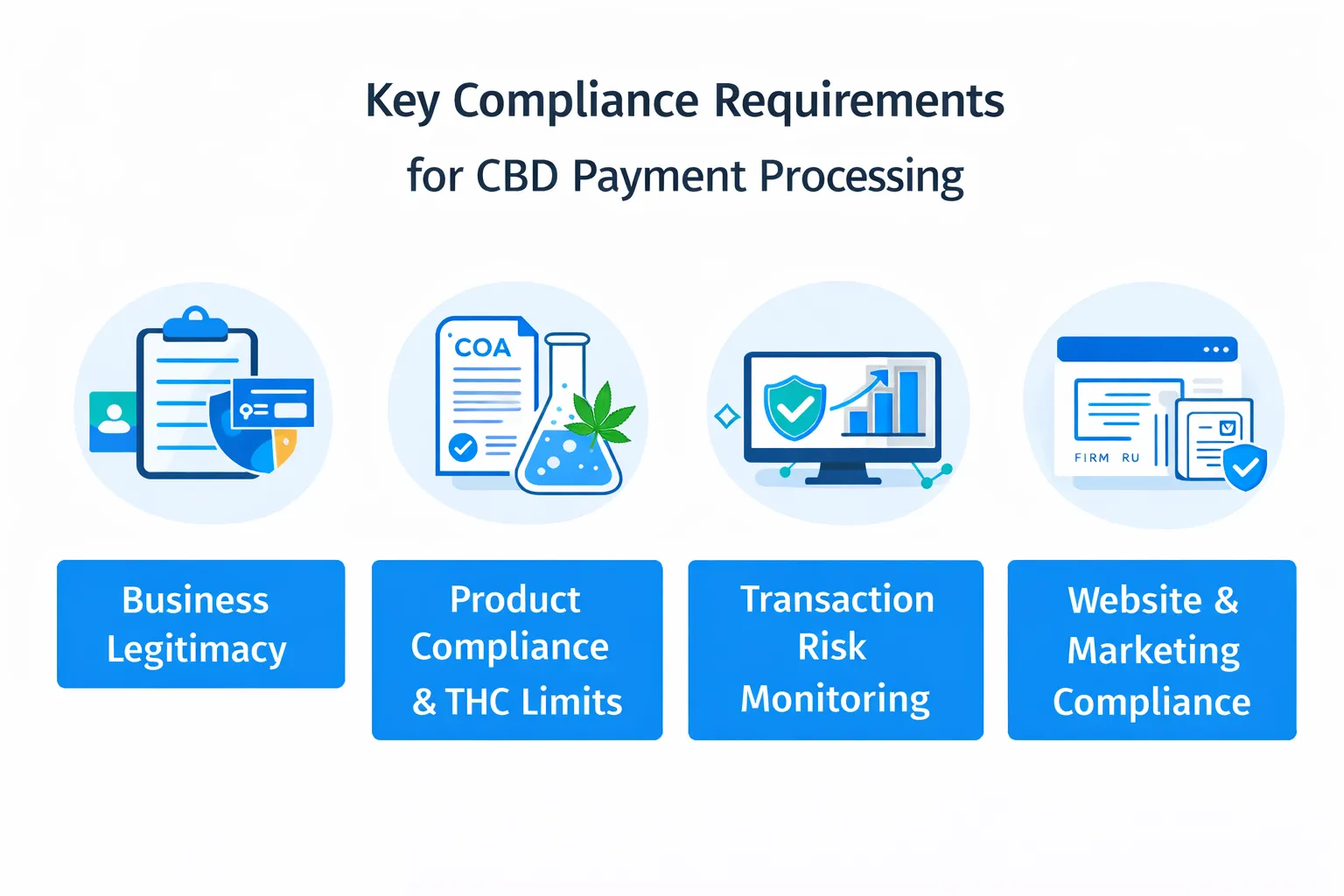

Key Compliance Requirements for CBD Payment Processing

For businesses, CBD payment processing approval largely depends on compliance readiness. Payment processors must verify that a CBD company operates legally and that its products meet regulatory standards. If compliance documentation is missing or unclear, the application is often rejected before onboarding even begins.

Most payment providers evaluate CBD merchants based on several key compliance checkpoints.

1. Business Legitimacy

Payment processors first verify whether the business is legally registered and authorized to operate.

Typical documents include:

- Company registration documents

- Business license

- Director or shareholder information

- Website and product listings

- Operating jurisdiction

These checks help financial institutions confirm that the merchant is a legitimate entity and not operating under misleading or unclear structures.

2. Product Compliance & THC Limits

CBD product compliance is one of the most critical areas of evaluation. Processors must confirm that products remain within legal THC limits and follow labeling rules.

Common requirements include:

- Certificate of Analysis (COA) from a certified laboratory

- THC percentage verification

- Ingredient disclosure

- Product classification (cosmetic, supplement, etc.)

For example:

These limits influence whether a payment provider can legally support the business.

3. Transaction Risk Monitoring

CBD merchants often operate through online stores and international shipping, which increases transaction monitoring requirements.

Processors typically evaluate:

- Chargeback ratio

- Refund frequency

- Monthly transaction volume

- Cross-border transactions

- Subscription or recurring payments

If chargebacks exceed card network thresholds (typically 0.9%–1%), the merchant may face account suspension.

4. Website & Marketing Compliance

Another area processors carefully review is the merchant's website and marketing claims.

They look for:

- Clear refund policy

- Terms and conditions

- Age verification where required

- No misleading health claims

- Transparent product descriptions

These factors help ensure the business does not violate payment network rules or consumer protection regulations.

Why Compliance Matters for Payment Approval

Many CBD businesses assume payment processors reject them because of the product itself. In reality, approval decisions are usually based on documentation quality and compliance transparency.

This is why many companies work with networks like FirmEU. Instead of contacting multiple providers blindly, businesses can connect with processors already familiar with CBD compliance requirements and transaction models. FirmEU facilitates introductions with verified payment partners that support CBD merchant account holders and understand their operational structure.

Also Checkout: Payment Localization Guide for International Businesses

Chargebacks, Risk Monitoring, and Transaction Compliance

For CBD businesses, payment processors do not only evaluate compliance during onboarding. They also continuously monitor transaction behavior and chargeback levels to ensure the merchant remains within acceptable risk thresholds. If unusual transaction patterns appear, processors may review or suspend the high-risk merchant account.

CBD merchants are often categorized as high-risk businesses, which means their transactions are monitored more closely than standard retail businesses. This happens because CBD products are frequently sold online, involve cross-border shipping, and sometimes attract higher refund or dispute rates.

Key Risk Metrics Payment Processors Monitor

Payment providers typically track the following indicators:

- Chargeback ratio – percentage of disputed transactions

- Refund frequency – how often customers request refunds

- Transaction velocity – sudden spikes in sales volume

- International transactions – cross-border payment patterns

- Recurring billing behavior – subscription or repeat payments

If these indicators exceed acceptable thresholds, the payment provider may flag the merchant account for further review.

Typical Card Network Risk Thresholds

Once a business crosses these thresholds, card networks such as Visa and Mastercard may classify the merchant as high-risk or excessive chargeback merchant, which can lead to penalties or account suspension.

How CBD Businesses Reduce Transaction Risk

CBD merchants can significantly improve payment stability by implementing proper risk management practices.

Some of the most effective measures include:

- Clear product descriptions to prevent customer misunderstandings

- Transparent refund and return policies

- Reliable shipping and delivery tracking

- Strong customer support channels

- Fraud prevention tools and payment verification systems

These steps help reduce disputes and keep CBD chargeback rates within acceptable limits, creating a more stable payment environment.

Why Risk Monitoring Matters for CBD Payment Processing

Payment processors prefer merchants that demonstrate predictable and compliant transaction behavior. When a CBD business maintains stable chargeback ratios and transparent operations, providers are far more likely to maintain long-term processing relationships.

CBD Payment Processing Models (Gateway, Acquirer, and PSPs)

To accept payments online, CBD businesses rely on a combination of financial infrastructure components. These components work together to process transactions, route funds, and ensure payments comply with regulatory and card network requirements.In many cases, CBD merchants must use a high risk CBD payment gateway because CBD transactions are commonly classified as high-risk by financial institutions.

Understanding how these systems work helps CBD merchants choose the right best payment processing company for CBD and avoid common processing issues.

Core Components of Payment Processing

CBD payment processing generally involves three main elements:

- Payment Gateway

The gateway captures customer payment details from the website and securely transmits the information to the payment processor. - Acquiring Bank (Acquirer)

The acquiring bank processes card transactions and connects the merchant to card networks like Visa or Mastercard. - Payment Service Provider (PSP)

PSPs combine multiple services such as payment gateways, fraud monitoring, and settlement management into a single platform.

Together, these systems create the infrastructure that allows a business to accept online payment processing for CBD.

Comparison of Payment Processing Components

Why CBD Businesses Need Specialized Processors

Many standard payment providers avoid CBD merchants because their internal risk policies do not support cannabis-related transactions. As a result, CBD companies often require specialized high risk CBD payment processors that already work with regulated industries and can support services such as a cannabis business bank account.

These processors understand the compliance requirements involved in CBD transactions, including THC limits, product documentation, and regulatory reporting.

Instead of contacting dozens of providers individually, many CBD companies choose to work with matchmaking platforms like FirmEU, which connect businesses with payment processors already experienced in handling CBD payment models and transaction structures. Through its network of verified partners, FirmEU helps businesses identify providers aligned with their business model and operating regions.

How FirmEU Helps CBD Businesses Access Payment Processing

For many CBD companies, the most difficult part of online payment processing for CBD is finding a provider willing to support their business model. Many businesses spend months contacting banks or processors only to face rejections due to internal risk policies or compliance uncertainty.

At FirmEU, we see this situation frequently. CBD companies often approach multiple providers individually, submit documentation repeatedly, and still struggle to find a stable payment partner. Instead of navigating this complex process alone, businesses can work with platforms that specialize in connecting companies with suitable financial partners.

FirmEU operates as an independent matchmaking platform that connects businesses with banks and payment processors already familiar with industries like CBD, crypto, e-commerce, and other regulated sectors. Rather than acting as a bank or payment processor, FirmEU focuses on identifying the best payment processing company for CBD and facilitating introductions.

The FirmEU Matching Process

The process generally follows three structured steps:

- Business Profile Review

The company shares details about its products, operating regions, and transaction structure. - Partner Matching

Based on this information, FirmEU identifies suitable providers from its network of 250+ verified banking and payment partners. - Direct Introductions

Once suitable matches are identified, FirmEU coordinates introductions between the business and selected providers.

Why CBD Businesses Use FirmEU

CBD merchants often choose FirmEU because it simplifies access to financial infrastructure that would otherwise be difficult to obtain.

Key advantages include:

- Access to processors familiar with CBD compliance requirements

- Connections to global banking and payment partners

- Reduced time spent contacting unsuitable providers

- Structured introductions aligned with the business model

Instead of approaching multiple processors blindly, CBD companies can focus on working with partners that already understand the regulatory and operational requirements of the industry.

This approach helps businesses build more stable payment infrastructure, especially when operating across multiple markets.

Looking for reliable CBD payment processing partners?

FirmEU connects CBD businesses with verified payment processors and banking partners experienced in regulated industries.

FAQs

Why are CBD businesses considered high-risk by payment processors?

CBD businesses are considered high-risk due to regulatory complexity, cross-border transactions, and higher potential for chargebacks or compliance issues.

How does FirmEU help CBD businesses with payment processing?

FirmEU connects CBD merchants with verified banks and payment processors that already support regulated industries.

Do CBD businesses need specialized payment processors?

Yes. Many traditional processors avoid CBD merchants, so businesses often work with providers experienced in regulated industries.

How can CBD businesses reduce payment processing risk?

Businesses can reduce risk by maintaining low chargeback ratios, transparent policies, and proper compliance documentation.

No. FirmEU is not a bank or financial institution. We operate as an independent matchmaking platform, connecting businesses with verified financial partners. All onboarding, KYC, and approval decisions are handled directly by the financial institution.

Still Have Questions?

Our sales team would be more than happy to assist with any futher inquiries

Contact Us

International Payment Solutions

Find the Right Banking and Payment Processing Partner for Your Business

Tell us about your company, and we’ll match you with the most suitable global banking or payment providers from our verified network.

Get Matched