6 Types of Cross-Border Payment Gateways Every International Business Should Know

Garry

March 9, 2026

1

minutes

Why Cross-Border Payment Infrastructure Matters for Global Businesses

In today’s digital economy, businesses are no longer limited to selling within their own country. An e-commerce brand based in Europe can sell to customers in Asia, a SaaS platform in the US can charge subscriptions globally, and a digital marketplace can receive payments from dozens of regions every day. However, once a business starts operating internationally, payments quickly become one of the biggest operational challenges.

Accepting international payments is not as simple as enabling a credit card gateway. Each region has different regulations, banking systems, currencies, and risk policies. Some payment processors may support local transactions but struggle with cross-border settlement, while others might restrict certain industries or regions altogether. As a result, many businesses experience issues such as:

- Failed international transactions

- Payment processor rejections

- Currency conversion complications

- Chargeback risks in foreign markets

- Limited support for local payment methods

This is where cross-border payment gateways play an important role. These gateways act as the financial bridge between a business and international customers. They enable companies to accept payments in multiple currencies, process transactions across different banking networks, and settle funds across borders. Whether a business needs a single international payment gateway or a broader cross border payment platform connecting several markets, the right setup depends on its specific operating footprint.

In simple terms, a cross-border payment gateway ensures that:

Without the right payment infrastructure, international businesses often face delays, declined transactions, or sudden account restrictions. This is especially common in industries with complex transaction patterns or global customer bases.

FirmEU frequently works with companies that are expanding internationally and struggling to secure reliable cross-border payment access. Through our network of 250+ verified banking and payment partners, we help businesses identify cross border payment companies and payment gateways that align with their industry, transaction model, and operating regions.

Read More: Payment Localization Guide for International Businesses

Expanding internationally but struggling with payment processing?

At FirmEU, we connect businesses with 250+ verified global banking and payment partners to help you access reliable cross-border payment gateways and international merchant accounts.

How Cross-Border Payment Gateways Work in International Commerce

Many businesses assume that a cross-border payment is simply an international version of a normal transaction. In reality, the process is far more complex. When a customer in one country pays a merchant in another, the transaction passes through several financial systems before the funds finally reach the merchant's account. Understanding how cross-border payments work at each stage makes it easier to see why some transactions succeed instantly while others stall or fail.

A typical cross-border payment involves multiple participants:

- The customer’s bank

- The payment gateway

- The acquiring bank

- The card network or payment network

- The merchant’s bank

Each of these entities performs specific verification and settlement tasks to ensure the payment is valid, compliant, and secure.

To make this easier to understand, here is a simplified flow of how an international payment works.

While this flow may look straightforward, cross-border payments introduce additional complexities such as:

Currency Conversion

When a customer pays in a different currency than the merchant’s settlement currency, the gateway must process foreign exchange conversion. Exchange rates and FX fees can significantly affect the final amount received.

Regional Payment Regulations

Every region has different financial regulations. For example:

- Europe operates under SEPA and PSD2 regulations

- The United States has card network and ACH frameworks

- Asia has local payment methods like Alipay, WeChat Pay, and UPI

Payment gateways must comply with these regulations to process transactions legally.

Risk and Fraud Screening

Cross-border transactions are statistically more likely to trigger fraud monitoring systems. Many payment processors apply stricter review policies to international merchants due to higher chargeback risks.

Settlement and Banking Infrastructure

Even after a payment is approved, funds must still move through banking networks before reaching the merchant’s account. Settlement times can vary from instant payouts to several days, depending on the gateway and banking partners.

This complexity is one of the reasons many international companies struggle to find reliable payment infrastructure. Different providers specialize in different transaction models, currencies, and industries.

Traditional Bank-Based Cross-Border Payment Gateways

Before fintech payment platforms became popular, international payments were almost entirely handled by banks. Even today, many global companies still rely on bank-based cross-border payment gateways, especially when transaction volumes are large or when regulatory compliance is critical.

In this model, the payment gateway is directly connected to a traditional bank or acquiring bank infrastructure. The bank acts as the core financial institution responsible for processing payments, settling funds, and managing currency conversions.

This structure is commonly used by:

- Large e-commerce companies

- International B2B trading businesses

- Import/export companies

- Financial institutions

- Companies handling high-value transactions

Because banks operate under strict regulatory frameworks, they typically provide stable and compliant payment infrastructure for global transactions.

How Bank-Based Payment Gateways Work

In a traditional banking setup, the payment process is tightly integrated with the bank’s financial network.

Once the payment is approved, the acquiring bank settles the funds into the merchant’s account after deducting applicable fees and FX conversions.

Payment Service Provider (PSP) Gateways for Global Transactions

Over the last decade, Payment Service Provider gateways have become one of the most widely used solutions for cross-border payments. Instead of relying solely on a single bank, PSP gateways combine multiple acquiring banks, payment networks, and processing technologies into one platform.

This allows businesses to accept international payments through a single integration, while the PSP manages the underlying payment infrastructure.

PSP gateways are commonly used by:

- SaaS companies

- Global e-commerce stores

- Subscription platforms

- Digital marketplaces

- Online service businesses

Because PSPs operate as intermediaries between merchants and financial institutions, they can often provide faster onboarding compared to traditional bank-based gateways.

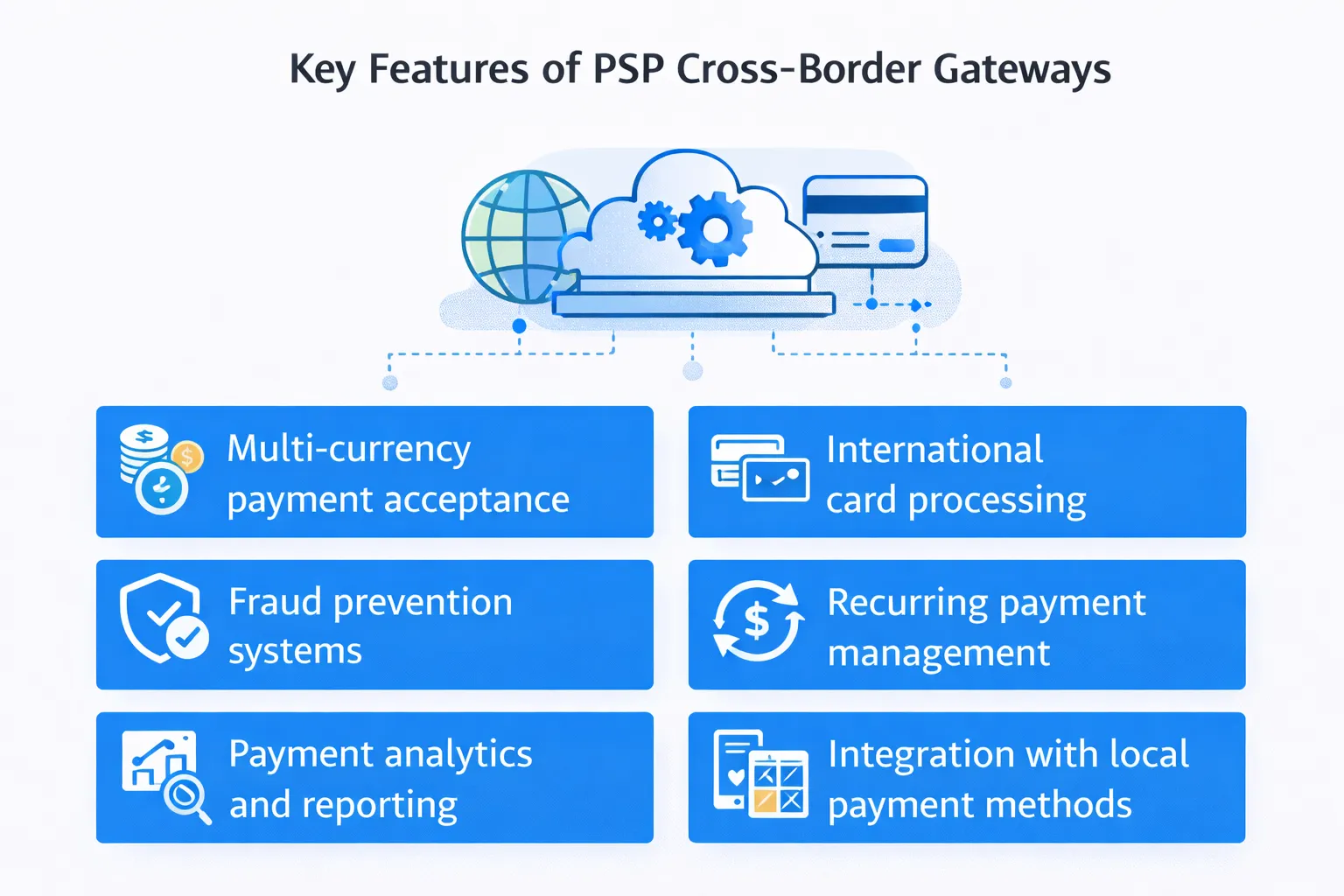

Key Features of PSP Cross-Border Gateways

PSP platforms are popular because they combine several payment capabilities into a single system.

Common features include:

- Multi-currency payment acceptance

- International card processing

- Fraud prevention systems

- Recurring payment management

- Payment analytics and reporting

- Integration with local payment methods

This makes PSP gateways particularly useful for businesses selling to customers in multiple countries.

Multi-Currency Payment Gateways and Global Merchant Accounts

As businesses expand internationally, managing multiple currencies becomes one of the biggest operational challenges. Customers expect to pay in their local currency, while merchants often prefer settling funds in their own base currency. This is where multi-currency payment gateways and global merchant accounts become essential.

A multi-currency payment gateway allows businesses to accept, process, and settle payments in multiple currencies without requiring separate payment systems for each region. Instead of forcing international customers to pay in a single currency, the gateway automatically handles currency conversion and settlement.

These gateways are widely used by:

- Global e-commerce platforms

- SaaS companies with international subscriptions

- Online marketplaces

- Travel and hospitality platforms

- Digital service providers

For businesses selling across multiple regions, supporting local currencies can significantly improve checkout conversion rates.

Key benefits include:

- Customers can pay in their preferred currency

- Higher checkout conversion rates

- Reduced payment friction for international buyers

- Ability to manage multiple currencies in a single platform

- Improved financial transparency for global operations

For example, a European e-commerce company selling to customers in the United States, Japan, and Australia may accept payments in USD, JPY, and AUD, while settling funds in EUR.

Local Alternative Payment Method (APM) Gateways

One of the biggest mistakes international businesses make is assuming that credit cards are the dominant and safest payment method everywhere. In reality, many countries rely heavily on local payment systems, digital wallets, and bank transfer methods that are different from global card networks.

This is where Alternative Payment Method (APM) gateways become critical for cross-border businesses.

An APM gateway enables businesses to accept region-specific payment methods that customers already trust and use regularly. Without supporting these local payment options, companies often lose a significant portion of potential customers at checkout.

Key advantages include:

- Higher payment acceptance rates

- Improved checkout conversion for international customers

- Access to local payment ecosystems

- Reduced dependence on credit cards

- Greater reach in emerging markets

For many regions, alternative payment methods account for a large percentage of online transactions, especially in Asia and Latin America.

High-Risk Industry Cross-Border Payment Gateways

Not every business can use standard payment gateways. Some industries are classified as high-risk by banks and payment processors due to regulatory complexity, chargeback rates, or reputational policies. Businesses operating in these sectors often find that traditional payment gateways decline their applications or restrict their accounts.

In these situations, companies must rely on specialized cross-border payment gateways designed for high-risk industries.How to Choose the Right Cross-Border Payment Gateway for Your Business

These gateways are built to handle complex transaction models and operate within strict compliance frameworks.

Industries Commonly Considered High-Risk

Certain industries are more likely to face payment restrictions because of regulatory policies or transaction behavior.

Examples include:

- Adult and dating platforms

- CBD and cannabis businesses

- Cryptocurrency companies

- Money Service Businesses (MSBs)

- Forex and trading platforms

- Subscription-based digital services

Many traditional payment processors apply strict internal policies toward these industries, which can make onboarding difficult.

How to Choose the Right Cross-Border Payment Gateway for Your Business

After understanding the different types of cross-border payment gateways, the next important step is selecting the one that aligns with your business operations. Many companies assume that the most popular global payment gateway will automatically work for them. In reality, the best payment gateway for cross border transactions depends on factors such as your industry, transaction model, operating regions, and compliance requirements.

Choosing the wrong payment infrastructure can lead to problems such as failed international transactions, unexpected account reviews, settlement delays, or even payment service termination.

To avoid these issues, businesses should evaluate several key factors before selecting a cross-border payment gateway.

1. Geographic Coverage

The first question to ask is whether the gateway supports the regions where your customers are located. Some payment providers specialize in specific markets, while others operate globally.

For example:

If your gateway does not support local payment networks, international customers may struggle to complete transactions.

2. Currency Support

Currency compatibility plays a major role in cross-border commerce. Businesses should ensure the gateway supports both customer payment currencies and merchant settlement currencies.

A good payment gateway should provide:

- Multi-currency payment acceptance

- Transparent FX conversion rates

- Flexible settlement options

Without proper currency support, businesses may lose revenue through unnecessary conversion fees.

3. Industry Compatibility

Some payment gateways restrict specific industries. Businesses operating in sectors such as digital services, subscription platforms, CBD, or adult entertainment may require specialized processors.

Choosing a gateway that already supports your industry can significantly reduce onboarding delays and operational risk.

4. Transaction Model

Your payment gateway should also match the way your business processes payments.

Common transaction models include:

- One-time product purchases

- Recurring subscription billing

- Marketplace payouts

- High-volume microtransactions

Each model requires different payment infrastructure and risk management capabilities.

5. Compliance and Risk Management

Cross-border payments are heavily regulated. A reliable gateway should comply with relevant financial regulations, including anti-money laundering (AML) rules and regional payment laws.

Gateways that maintain strong compliance frameworks typically provide:

- Fraud detection systems

- Chargeback management tools

- Secure payment encryption

- Regulatory reporting support

These features help protect both the business and its customers.

Why Many Businesses Seek Expert Guidance

Even after evaluating these factors, many companies still struggle to identify suitable payment providers. The cross-border payments ecosystem includes thousands of banks, processors, and fintech platforms, each with its own policies and onboarding requirements.

At FirmEU, we help businesses simplify this process. Instead of approaching providers individually, companies can access structured introductions to payment partners that align with their business profile. Through our network of 250+ verified global banking and payment providers, businesses can identify solutions designed for international operations and cross-border transactions.

Cross-border payment gateways play a crucial role in enabling businesses to accept payments from customers across different countries, currencies, and financial systems. Choosing the right gateway depends on factors such as industry, transaction model, and regional payment infrastructure.

At FirmEU, we help global businesses connect with suitable banking and payment partners through our network of 250+ verified financial institutions, simplifying access to reliable cross-border payment infrastructure.

Need a Reliable Cross-Border Payment Gateway?

Finding the right international payment provider can be complex due to regulatory requirements, banking policies, and regional restrictions.

FAQs

Why do businesses need international payment gateways?

Businesses selling globally need these gateways to process payments in multiple currencies and comply with international payment regulations.

Are cross-border payments more risky?

Yes, international payments often carry higher fraud and chargeback risks compared to domestic transactions.

What industries need high-risk payment gateways?

Industries like CBD, cryptocurrency, forex trading, and adult platforms often require specialized high-risk payment processors.

How do businesses choose the best cross-border payment gateway?

They should evaluate geographic coverage, currency support, compliance requirements, transaction models, and industry compatibility.

How long do cross-border payments take to settle?

Settlement times vary from instant payouts to several days depending on the payment gateway and banking infrastructure.

No. FirmEU is not a bank or financial institution. We operate as an independent matchmaking platform, connecting businesses with verified financial partners. All onboarding, KYC, and approval decisions are handled directly by the financial institution.

Still Have Questions?

Our sales team would be more than happy to assist with any futher inquiries

Contact Us

International Payment Solutions

Find the Right Banking and Payment Processing Partner for Your Business

Tell us about your company, and we’ll match you with the most suitable global banking or payment providers from our verified network.

Get Matched